Officials Provide Updates on Repurchases, ADUs, Outlooks at MBA Annual

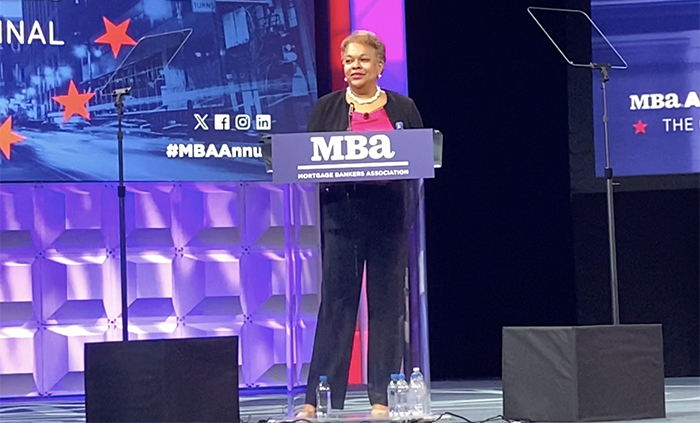

(Thompson speaks on stage. Picture by Anneliese Mahoney)

PHILADELPHIA–A slate of federal officials took to the stage to provide updates at the Mortgage Bankers Association’s Annual Convention & Expo here Oct. 16.

For one, Federal Housing Finance Agency Director Sandra Thompson announced that the agency has directed the enterprises to extend their rep and warrant policies for loans that have been affected by natural disasters to cover mortgages that have successfully exited a COVID-19 forbearance.

The policy will take effect at the end of October.

Thompson also said, “we remain open to additional options that will ensure alternatives to repurchases are available and that they’re offered on a regular basis, and work on this front remains ongoing.”

In response to the announcement, MBA President and CEO Robert Broeksmit, CMB, released a statement that said in part: “MBA has advocated strongly for FHFA to address the GSEs’ increased incidence of loan repurchase requests–especially for performing loans and those with relatively minor issues underwritten during the pandemic. We share FHFA and the GSEs’ goal of high-quality underwriting and will continue to work with them to ensure the rep and warranty framework is being applied in a balanced way, and that there are appropriate alternatives that lead to outcomes short of a repurchase request.”

“FHFA’s policy change to provide rep and warrant relief for performing seasoned loans that have successfully exited COVID-19 forbearance plans is a longstanding recommendation that we are pleased to see implemented,” Broeksmit continued.

In other FHFA news, Thompson noted that the agency continues efforts related to appraisal data. At last year’s MBA Annual Convention & Expo, Thompson announced the release of the uniform appraisal dataset, featuring aggregate statistics.

“One year later, I’m pleased to announce that we’re releasing data at the appraisal level for the first time,” Thompson said. “This data will allow stakeholders to assess appraisal issues as never before within the framework of our laws that also support a consumer’s right to privacy.”

FHA Commissioner Julia Gordon also took to the podium for updates. She announced the release of a brand new policy from her agency pertaining to single-family homes with accessory dwelling units, allowing for the inclusion of rental or prospective rental income when underwriting a mortgage.

This will allow more borrowers to purchase properties with ADUs and construct more new homes with ADUs. Gordon noted it will help boost the affordable housing stock.

Gordon also provided an update of a new option for loss mitigation–the payment supplement partial plan. “That would allow a borrower to use available partial claim funds to subsidize their monthly mortgage payment for a period of time to get that payment reduction effect that we know is the key to sustainability for loss mitigation efforts,” she said.

Gordon said she hopes there will be a final policy out before the end of the year–although issues such as another potential lapse in appropriations loom large.

Conference attendees also heard from Patrick Harker, President and CEO of the Federal Reserve Bank of Philadelphia. As high rates have weighed on the industry, Harker said he personally believes the Federal Reserve is at a place where it can hold rates where they are.

How long they will remain high, however, Harker declined to say.

“As time goes on, as adjustments are completed, and as we have more data and insights into underlying trends, I may need to adjust my forecasts and with them my timeframe,” Harker said. “But as for future policy, I can tell you that I do subscribe to the moniker ‘higher for longer.’ ”

Consumer Financial Protection Bureau Director Rohit Chopra engaged in an on-stage discussion with MBA’s Broeksmit. They touched on items ranging from the CFPB’s status–and the pending Supreme Court case–to the potential of a servicing rulemaking in 2024. (Earlier this year, the Mortgage Bankers Association, the National Association of Home Builders and the National Association of Realtors filed an amici brief with the U.S. Supreme Court in Consumer Financial Protection Bureau v. Community Financial Services Association of America. While the brief takes no position on whether the Bureau is constitutionally funded, it urges the Court to avoid ruling in a manner that would disrupt the housing and mortgage markets, harming both consumers and the economy.)

One hot topic is concern that the Financial Stability Oversight Council could designate non-banks as systemically important, prompting greater regulatory scrutiny. Broeksmit pressed Chopra on that potential.

“It’s an important industry for the entire economy,” Chopra noted, saying that when non-banks fail, that can have far-reaching ramifications. Chopra also highlighted concerns over, for example, activities outside of the normal banking system, such as new kinds of payment systems and coins.

“I don’t want you feeling the mortgage industry is under some special, you know, magnifying glass, it’s really the entire shadow banking arena to make sure that we understand and can mitigate those risks,” Chopra said.