Mark Dangelo: Innovation Thinking—Winning in an Uncertain Future

Mark P. Dangelo is president of MPD Organizations LLC and an adjunct professor of graduate studies in innovation and entrepreneurship at John Carroll University. He is the author of four innovation books and numerous articles. Mark is a strategic management consultant, operations advisor and leadership specialist with extensive process, technology, and financial experience, and he is a frequent contributor to MBA NewsLink. He can be reached at mark@mpdangelo.com or at 440/725-9402.

Dangelo

It is an odd-topic to be sure—innovative thinking. At a time when mortgage availability has fallen more than 26% (per the #MBA) in two months and credit standards have risen to 2008 levels, the thought of thinking innovatively is likely not proceduralized within the corporate agenda. Yet, innovative thinking to deal with unprecedented challenges and choices is exactly what is being attempted to deal with the calamitous global shock now confronting consumers and their economies.

Indeed, the past few months have been horrid—COVID-19 enters from stage left ripping into social structures and businesses with tidal waves of destruction. It is as if mountainous boulders were dropped in large bodies of water, and the outward ripples engulfed anything in its path including employment, travel, finances, social interactions, public benefits and sovereign economics.

The implications of the viral pandemic are still being tabulated, written if you will, as the world anxiously awaits a second coming during a U.S. Presidential election cycle, which will likely further social and cultural divisiveness and discord. If we were not questioning how to adapt your business to new markets before, you now realize you have no choice. Yet, can this gloom and upheaval result in an explosion of new, demanded innovative thinking that will spur a lasting economic recovery?

It is against this backdrop of uncertainty and chaos where businesses must operate within a “normal” that is anything but familiar. In fact, do we really comprehend what “normal” will even represent? The models we operated within and against are broken, and the supply chains, so common and honed on global delivery, have been exposed for their lack of redundancy, failure to possess contingency options, and rampant hegemony which proceduralized vulnerabilities, inequalities, and disparities.

Moving forward, we recognize that the “next normal” will have many functional elements very foreign to our cultures and principles, which must be addressed to ensure responsible rigor and discipline in the face of global chaos. Today, with declines in profitability and the increasing likelihood of rising loan defaults now a certainty just as recessionary and inflationary impacts unfold (see the recent series “Are Bankers Necessary”), what will bankers do to promote and accept sustainable innovative thinking?

Anticipate Failures, Expect Delays

The divide between aspiration and innovation is growing. Within financial services and banking organizations, there is a need to bridge the expanding gap between creativity and delivering a path for sustainable accomplishment. Innovation as a term, analogous to a person who constantly curses using the same word as a noun, verb, adjective, and adverb all within the same sentence, is an increasingly meaningless descriptor now used to justify any initiative outside of the current corporate vernacular. Now with current events breaking business models, sinking value propositions, and alienating customers, there are many questions that must be asked (before a prescriptive answer is accepted) to determine the journey forward.

For example, is #COVID-19 the “wake-up call” that many economist and strategist have been touting since the Great Recession that will permanently alter economies? Is it a balancer of wages, equality, and wealth? Will the pandemic responses now lead to a series of unintended consequences (e.g., a recent $5 billion margin call for mortgage firms) which will sideline recovery—energy, leisure, lending, retail, education, agricultural, and governments (state and local)? Moreover, does the global pandemic point to a fallacy of innovations that are concentrated on services, and not products, which are in the end needed to adequately respond to markets turned inward (e.g., domestic supply chains)?

However, for financial services and banking organizations (#FSBOs) the questions of how consumers will respond and the downstream impacts on their habits are emerging and representing significant risks. These risks include politically introduced forbearance (>7% of borrowers), rental non-payments, educational loan defaults, credit card and auto loan delinquencies, and a lack of income to sustain living conditions (with over 33 million unemployed). When it comes down to it, what is the exposure within existing loans, and will it require a revisiting of what constitutes a qualified buyer?

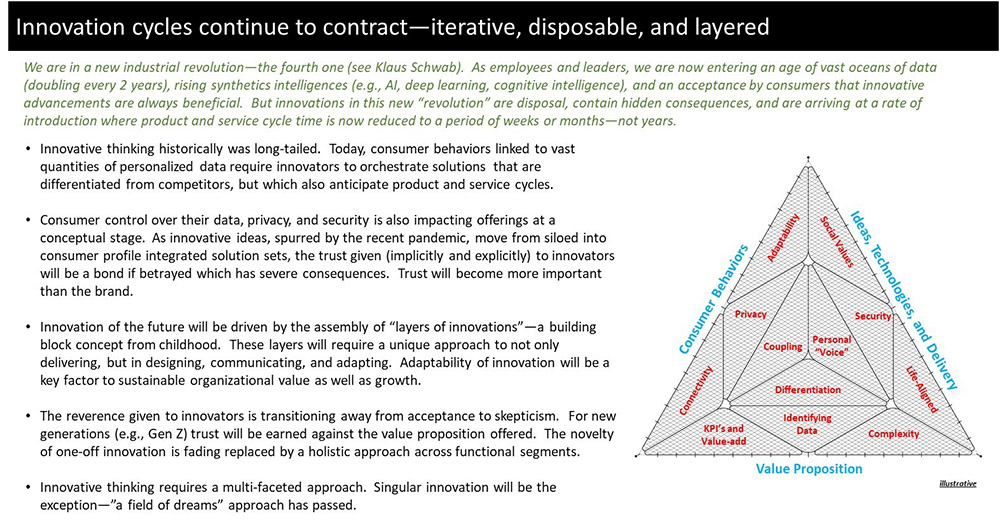

The following panel highlights the changes occurring and the challenges ahead when it comes to internalizing innovative thinking within the enterprise during times of uncertainty.

Indeed, the concept of teaching innovative thinking appears tangentially oxymoronic. How can enterprises teach, accept, and integrate innovative thinking as part of economic transformation—when none of the traditional rules apply? We need to internalize that not everyone is innovative. Not all organizations allow for innovative thinking. Innovative thinking is far more than a concept or an articulation of an idea (we all have ideas)—it is a skill that when taught, can reward individuals and enterprises with significant competitive advantages.

Moreover, all this chaos and the unpreparedness of supply chains and business practices begs a few more “common sense” questions. Will these events ultimately lead to dreaded inflation, or perhaps worse, deflation like the lost decades economies like Japan experienced with interdependent governments drowning in debt?

And, as the mortgage world begins to assess the impacts to their loans, their consumers, and their investors, where will those fickle, fair-weather politicians decide that somethings are not worthy of financial rescue? Finally, as industry news focuses on standardized closing, e-“solutions”, robotic process automation (#RPA), and COVID-19 “best practices”, is there an unwritten category of “is this enough” using the traditional market approaches need to be captured? Or, does all this signal the start of a new cycle which requires vastly unique innovative thinking and operating practices not beholden to our desire for standardization (which has promoted information interchanges)?

Time to Re-Examine the Future

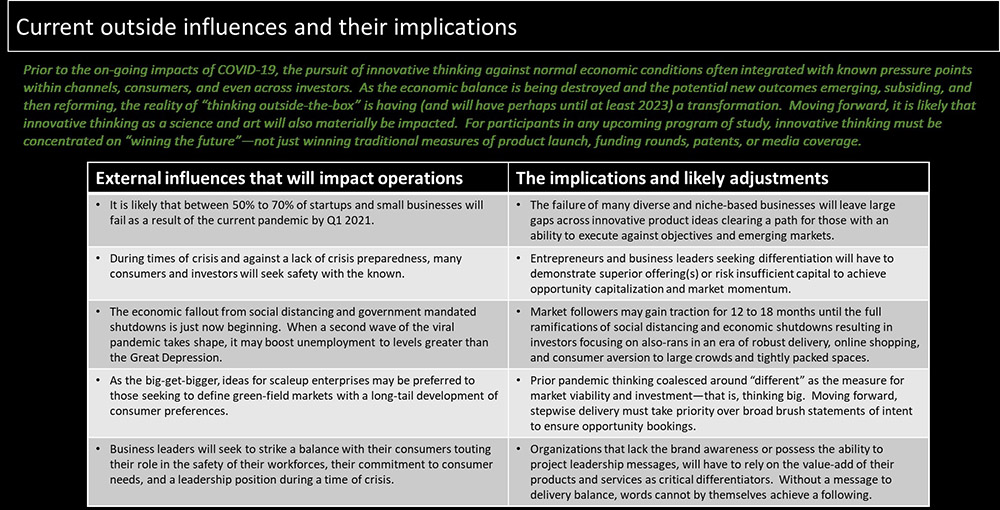

The impacts of the continuing pandemic will continue with the rising deaths of more than 80,000 Americans (as of this writing), more than 33 million unemployed, a retail industry unlikely to ever recover losing more 25% of their jobs permanently (see The Atlantic, “The Pandemic Will Change American Retail Forever” and National Retail Federation), and the unknowns of lasting consumers behaviors during and after it all (e.g., will they ever go back in mass to dine-in restaurants)? Current behaviors are being altered and their next iterations are now suggestively being married to tracking software and opaque public surveillance methods (i.e., acceptance of intrusive privacy violations and individual movement restrictions under the banner of public good under the watch of congressional bills proposing 750,000 “enforcers”).

As behaviors shift, what will these external factors do to our business models? How will these alterations and adoption of new impact our value equations—or are we expecting innovation to be a panacea shield against failures? More importantly, since our firms already operate in the “real world” with offerings and obligations, how are we marking and incorporating feedback which fundamentally requires radical shifts to deliver customer needs while capitalizing on opportunities. Let us review a snapshot of what transforming right in front of us in the panel below.

“Staying in your lanes” used to be operating principles that allowed for niche specialization, which for astute entrepreneurs, defined new innovative markets within finance and especially within mortgage. After the Great Recession when many large FSBOs exited the home loan markets as well as private securitizations, new lending businesses not governed by the traditional thinking of banking dogma rose. These institutions originated, prior to the pandemic, more than 75% of the conforming loans and over 90% of the non-conforming residential loans. By numerous estimates, similar institutions controlled one-tenth of these issuances before 2008.

Now these very new age institutions that dominated these once traditional markets for the last decade are themselves being forced into innovation thinking challenges with cultures defined by their aggressiveness and delivery models of innovative offerings. Will these cultures, now foundationally delineated to their own operating models and offerings, be able to anticipate the markets, fail quickly (if it is required), and transform rapidly, while accepting the likely explosion of servicing related challenges across the complex financial supply chains (using reverse orchestration back into the originating transactions and activities)?

Overcoming Organization Design, Cultural Limitations and the Calamity of Politics

Minimally, the pandemic has reinforced the demand for robust crisis management after a decade of prosperity. Innovations that were marginal before markets froze and funding retreated, and are among the dozens per day that are being shuttered. Innovative passion is not a substitute for sustainability or pragmatism during these times of turmoil.

Within the graduate courses on innovation and entrepreneurship that I teach, participants are being taught to assume that proven innovation delivery models will be questioned, axioms will be displaced, and models of business model formation will be shelved. Any innovative thinking, seeking market acceptance, must demonstrate and realize viability in times of unprecedented risks and political turmoil.

Just as consumers can bond with their innovations, innovators and their hand-picked teams can also become myopically driven into conclusions because of their personal passions and environmental biases. What is painfully obvious, is that innovative thinking requires not only the context and tools needed to hone market offerings, but also the innate questioning to destroy what one has already “built”. Meaning, an inability to challenge existing accomplishments, even if successful, can result in innovative disruption being comprehensively disrupted.

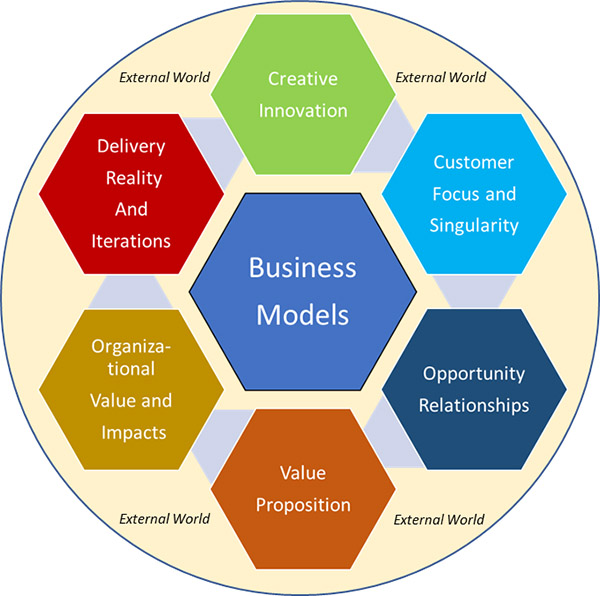

All these factors impact the enterprise offerings across seven functional categories—six of which revolve around the now changing business model(s) deployed across a FSBO. The following illustration, which is part of a semester long class graduate class on innovative thinking, highlights the skills needed and the impacts it has on solutions moving forward.

An analogous elucidation would be the emerging use of “edge” computing layers to incorporate innovative thinking into the infrastructure. Edge computing and its architecture is moving from a monolithic design into one that is hybrid based tightly coupled to #IoT and #5G. The new approaches are distributed, possessing cloud and localized capabilities all linked to form a dynamic offering that is not restricted by precedence or expectations.

This “edge” delivery approach represents innovative thinking that meets many objectives, while limiting the risks associated with non-layered implementations. By recognizing that all its components have touchpoints, the adjustments and innovations can be compartmentalized, reworked, and integrated with shorter timeframes, larger data pools, and higher quality of output. This example is innovative thinking that alters the business model, exploits the opportunity, and creates a new value proposition that satisfies changing customer requirements.

The business and organizational models that once were common paths to transform innovative thinking into workable business models, are increasingly becoming be non-viable especially in a decade prior to the pandemic that already demanded vast reskilling of U.S. workforces (see “The Challenges of Reskilling Work Forces” series). New approaches and harsh realities will force entrepreneurs and transformation leaders to move beyond innovative fantasy goals into incremental ones as the runways traditionally used to gain critical mass are shortened.

In summary, Pollyanna, rainbows and unicorns have little to do with this critical skill (i.e., innovative thinking) required for FSBO leadership in crisis and contemplating post-pandemic operations. Moreover, we are in an era when nothing, and I mean nothing can be switched off resulting in oceans of data, and a demand to predict what comes next. Innovative thinking has little to do with age, social status, wealth measurements, educational background, or dare I say, technological offerings. Innovative thinking always requires applicability to customers and solving pain-points (i.e., voids), while delivering insights, defining the value-add, and capitalization of emerging opportunities.

Thinking innovatively is not inherent in everyone’s DNA, but with training and augmentation those traits can be transplanted into corporate cultures thereby providing lasting sustainability—crisis or not. This is the challenge and opportunity for all FSBOs—to accept that innovative thinking is a skill to be learned and nurtured during a time of uncertainty.

The winners of the future will be those leaders who can deliver the training and education to their staffs and partners on how to channel ideas into reality. To win in an uncertain future, FSBOs must look beyond budgets, look beyond their assumptions, look beyond their limitations, and look beyond their feeling that “we’ve got this covered”.

(Views expressed in this article do not necessarily reflect policy of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes your submissions. Inquiries can be sent to Mike Sorohan, editor, at msorohan@mba.org; or Michael Tucker, editorial manager, at mtucker@mba.org.)