Your HMDA Data Is Telling You More Than You Think: A Practical Path to Profitable, Inclusive Purchase Growth

Laird Nossuli is CEO of iEmergent, Urbandale, Iowa; Rob Chrane is CEO of Down Payment Resource, Atlanta.

Affordability pressures are reshaping the purchase market in ways many lenders still underestimate. While HMDA data is often viewed through a compliance lens, it also offers a clear, retrospective view of where affordability breaks down—who is being denied, why they are falling out of the funnel and where qualified demand is being left untapped. Analyzed alongside current affordability and assistance data, HMDA points to a practical path forward: using existing tools to expand purchase volume among low- and middle-income borrowers without sacrificing profitability.

—

The U.S. housing market has reached a point where home prices are no longer aligned with household incomes, fundamentally changing who can afford to buy and how lenders must think about qualification and growth.

In 2024, the national home price-to-income ratio reached 5.0, matching record highs and far exceeding historical norms, according to the Joint Center for Housing Studies at Harvard University. Home prices have risen roughly 60 percent since 2019, while incomes have failed to keep pace, pushing affordability well beyond traditional lending assumptions. A typical first-time homebuyer now needs an annual income of at least $126,700 to afford the median-priced home, yet only one in seven renter households earns enough to meet that threshold.

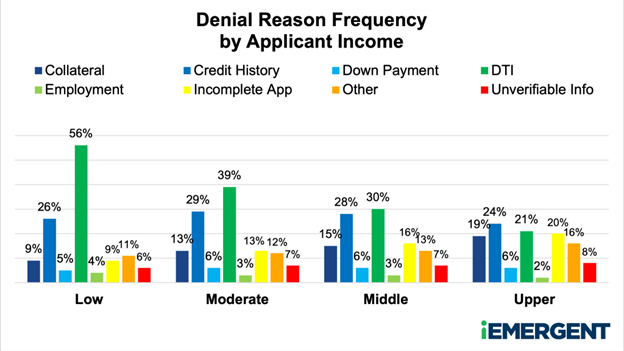

That shift is already evident in Home Mortgage Disclosure Act (HMDA) data. An iEmergent analysis shows debt-to-income (DTI) ratios have emerged as the primary driver of denials—not only for low-income applicants, but also for moderate- and middle-income households whose purchasing power has been eroded.

Down Payment Assistance Is Being Underutilized

Down Payment Resource’s Declined Loan Analysis shows these outcomes are often avoidable. By matching declined applications against more than 2,600 homebuyer assistance programs, DPR found that up to 40% of declined loans were eligible for at least one assistance option. More striking, 89% of purchase loans declined for cash-to-close or DTI reasons could potentially have been salvaged with the right down payment assistance. On average, declined applications were eligible for 10 homebuyer assistance programs.

This is not a niche solution: 62% of assistance programs allow household incomes above $100,000, and applying the best available program reduced loan-to-value (LTV) ratios by an average of 8.8%—up from 6% in prior years.

These data points reveal a critical disconnect. Affordability has shifted structurally, but lending strategies have not fully adapted to it. For lenders, the challenge is recognizing how much opportunity is being left on the table.

The Missing Middle: What HMDA Data Reveals About Today’s Borrowers

Affordability pressures are no longer confined to the lowest end of the income spectrum. iEmergent’s analysis of national denial patterns shows that, for both moderate- and middle-income borrowers, denials are most frequently driven by DTI ratios—39% for moderate- and 30% for middle-income groups. Relatively small reductions in loan-to-value, often achievable through existing assistance programs, can be enough to move them from denial to approval.

It is also important to note that many affordability constraints, particularly related to cash-to-close, surface earlier in the homebuying process and influence whether households move forward at all, a form of silent attrition that is difficult to quantify and does not appear in denial-reason data.

At the same time, middle-income households are increasingly priced out or outcompeted, particularly in higher-cost markets. As home prices continue to rise, assistance programs serving up to 100–120% of the area median income have become essential to sustaining purchase activity across many geographic areas. What was once considered targeted support has become a necessary affordability tool for a much broader segment of the market.

Invisible Demand: When Affordability Keeps Borrowers From Applying

Denial data alone understates the true scale of the problem. Many lenders report low denial rates not because affordability barriers are limited, but because large numbers of otherwise eligible households never apply. Some of this appears in HMDA as withdrawals, but much of it remains invisible. Millions of households assume homeownership is out of reach and self-select out before entering the application funnel.

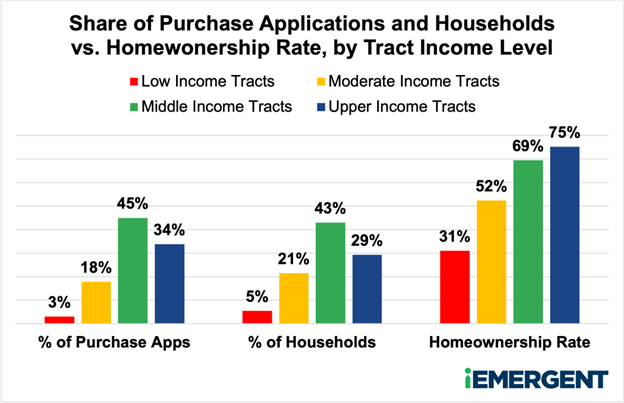

iEmergent’s analysis highlights a clear discrepancy between applications and demographics: while middle-income households account for roughly 43% of U.S. households, they represent only about 24% of mortgage applications, signaling substantial untapped purchase demand.

Geographic dynamics further intensify the challenge. Affordability constraints vary widely even within a single metro, as lower-priced inventory disappears and new construction increasingly targets price points beyond the reach of even middle-income buyers.

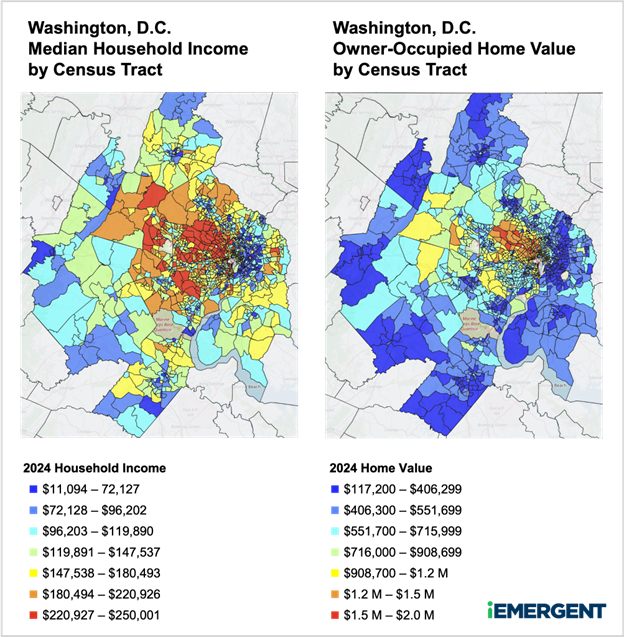

Washington, D.C. serves as an example of an uneven affordability landscape, with the highest home values concentrated in the urban core and close-in suburbs, while lower-priced areas are pushed farther outward. Income patterns mirror this divide, with middle-income households earning roughly $96,000 to $147,000 scattering transitional and outer regions alongside low- and moderate-income households.

Why Serving Low-, Moderate- and Middle-Income Borrowers Strengthens Profitability

Rising home prices have pushed affordability barriers well into the middle of the income spectrum, making middle-income households a critical and often overlooked source of purchase demand. Broadening eligibility to include this population, alongside low- and moderate-income households, reduces friction, re-engages sidelined buyers and expands volume in a constrained market.

Inclusive assistance strategies also strengthen community and market goodwill. When affordability solutions are positioned as broadly available tools rather than narrowly targeted subsidies, they resonate across income levels, demographic groups and political lines, expanding buy-in and reinforcing a lender’s role as a trusted, long-term partner in local housing markets.

Assistance should be viewed as a growth engine, not a niche product. Its availability brings households into the pipeline earlier, even when they do not ultimately use it, expanding reach and deepening engagement. Over time, these relationships translate into durable value through retention, deposits and repeat business.

Building assistance capabilities that serve middle-income borrowers strengthens the entire organization. The same data discipline, program alignment and execution required to support middle-income households naturally extends to low- and moderate-income markets, creating a consistent, repeatable model for sustainable growth.

Turning Affordability Data Into Actionable Growth Strategies

Lenders can start by using HMDA data to identify where DTI pressure, cash-to-close gaps and denials reflect solvable affordability barriers, then align those insights with existing down payment and closing-cost programs that are often underutilized. Where gaps remain, local data can inform targeted solutions—such as special-purpose credit programs or lender-funded assistance—reinforced through engagement with community partners.

This is not a concessionary strategy. By reducing debt-to-income and loan-to-value ratios, assistance unlocks approvals, stabilizes pipelines and supports long-term profitability in an affordability-constrained housing market.

The opportunity lenders are searching for is already visible in their data. HMDA clearly shows where affordability is limiting approvals and where qualified demand is being left untapped. These pressures are structural, driven by lasting shifts in home prices and incomes, and they require strategies that move beyond legacy assumptions.

Lenders that rethink borrower eligibility, fully leverage existing assistance programs and use data to guide targeted, market-specific solutions will be best positioned to capture sustainable purchase share. The tools already exist. The leadership moment is deciding to use them.

(Views expressed in this article do not necessarily reflect policies of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes submissions from member firms. Inquiries can be sent to Editor Michael Tucker or Editorial Manager Anneliese Mahoney.)