CFPB: Mortgage Servicers’ Pandemic Response Varies Significantly

The Consumer Financial Protection Bureau on Tuesday published a report detailing 16 large mortgage servicers’ COVID-19 pandemic response. The report showed a disparate response in call metrics, exit metrics and other measures.

The report’s data metrics include call handling and loan delinquency rates, highlighting what the Bureau said was the servicing industry’s “widely varied” response to the pandemic.

For example, the report said many servicers managed to handle high call volume with an average hold time below 3 minutes, while others reported keeping callers waiting for as long as 26 minutes.

The CFPB used supervisory data from 16 large servicers to understand how they are interacting with homeowners during the pandemic and whether those interactions are effective. The monitored key data metrics, including:

• Call metrics to understand how servicers managed the volume of homeowner calls. The metrics in the report include Average Speed to Answer and Abandonment Rates a measure of how many borrowers disconnect from servicing calls prior to completion. Most servicers reported abandonment rates of less than 5% during the reporting period, while others exceeded 20%, and one peaked at 34%.

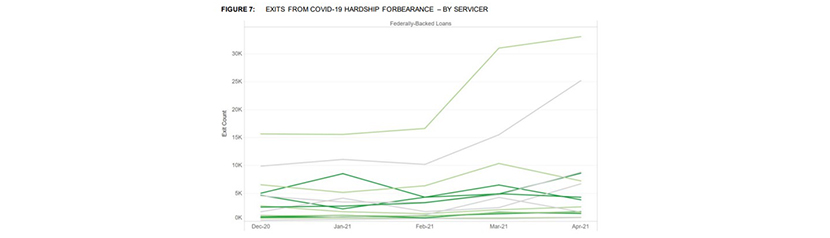

• Pandemic forbearance exit metrics to determine the support provided to homeowners transitioning out of COVID-19 hardship forbearance programs. Many servicers saw increased delinquent exit rates in March and April 2021, and some servicers were clear outliers. For federally backed loans, three servicers, which used the same sub-servicer, had relatively higher delinquent exit rates for one or more serviced portfolios – consistently exceeding 50%.

• Delinquency metrics to identify, among other things, variation of homeowner delinquency rates among servicers. Overall delinquency rates ranged from about 1% to 26% for both federally backed and private loans. (Differences in delinquency rates may reflect the differing composition and risk profile of each servicer’s portfolio.)

• Borrower profile metrics to determine whether and how servicers track borrowers’ race and limited English proficiency status. Nearly half of servicers in the report clearly stated that they did not collect or maintain information about borrowers’ LEP status, which may lead to borrowers not receiving needed language assistance. Some of the servicers also reported not maintaining data on borrowers’ race, which may raise the risk of fair lending violations.

• Pandemic assistance enrollment metrics to understand the types of assistance programs offered to homeowners and whether homeowner applications to those programs were accepted or rejected. Forbearance was widely available for borrowers with both federally backed and private loans, and the reported denial rates were consistently low for both loan types.

CFPB Acting Director Dave Uejio said the Bureau expects servicers to compare the report’s findings to their own internal metrics to identify opportunities for, and demonstrate concrete efforts toward, improvement.

“Many emergency mortgage protections are winding down, and servicers have had ample time to prepare for the millions of distressed homeowners who need their assistance,” Uejio said. “Today’s report should inform servicers’ own data reviews as they determine whether they are doing enough for borrowers. Servicers who find themselves at the bottom of the pack should immediately take corrective steps. The CFPB will hold accountable those servicers who cause harm to homeowners and families.”

The report can be found here.