“Without proper calibration of these requirements, unintended consequences likely would include more institutions selling loans only through the cash window rather than an MBS execution, shifts in volume away from the Enterprises or Ginnie Mae for reasons that are not determined by market conditions and potential consolidation in the industry, resulting in fewer choices and higher costs for borrowers. Proper calibration of these requirements, on the other hand, will promote resiliency in the market and broad, sustainable access to credit for consumers.”

–From an MBA letter to the Federal Housing Finance Agency on its re-proposal of servicer eligibility requirements for loans backed by Fannie Mae and Freddie Mac.

Category: News and Trends

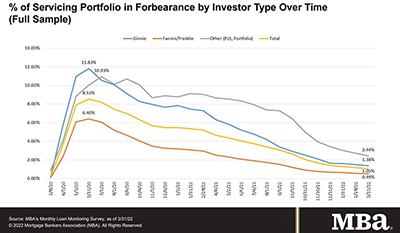

MBA: Share of Mortgage Loans in Forbearance Decreases to 1.05%

Loans in forbearance fell to another pre-pandemic low to just barely above 1%, the Mortgage Bankers Association reported Monday.

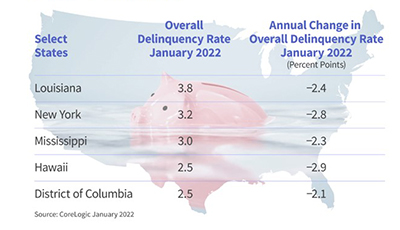

CoreLogic: Mortgage Delinquencies at 23-Year Low

CoreLogic, Irvine, Calif., said mortgage delinquencies fell in January to their lowest level since 1999.

#MBATech2022: ‘The Digital Future Is Drawing Closer’

LAS VEGAS—A byproduct of the coronavirus pandemic: the real estate finance industry adopted innovative technology solutions with extraordinary speed. Now, said Mortgage Bankers Association Chair-Elect Matt Rocco, the industry must take the next step.

#MBATech2022: View from the C-Suite: ‘You Have to Try New Things’

LAS VEGAS—Executives here at the Mortgage Bankers Association’s Technology Solutions Conference & Expo said the biggest lesson from the coronavirus pandemic: don’t let your company sit still.

#MBATech2022: Mortgage Industry Faces Growing Security Risks

LAS VEGAS—Security risks don’t just mean breaches and ransomware. Increasingly, individuals and companies are losing money due to wire fraud and other attacks.

FHFA Issues 2022-2026 Strategic Plan

The Federal Housing Finance Agency, Washington, D.C., released its 2022-2026 Strategic Plan last Thursday.

#MBATech2022: How Trends Intersect in a Changing Industry

LAS VEGAS—Real estate finance has migrated quickly from a person-to-person business to a person-to-tech-device-to-person business. And socio-economic forces are rapidly steering technology to reshape business—even as business continues to fine-tune technology.

#MBATech2022: Where We Are on the Digital Journey

LAS VEGAS—We have been hearing about digitalization of mortgages for years. What has been successful, and what has fallen short? Are lenders’ real-world results living up to the hype?

MBA Education Fundamentals of Mortgage Banking for Secondary Marketing Professionals Virtual Workshop May 9

MBA Education presents a virtual workshop, Fundamentals of Mortgage Banking for Secondary Marketing Professionals, on Monday, May 9. Join MBA Education for a virtual workshop tailored specifically for Secondary Marketing …