Chart of the Week: Total Commercial Real Estate Lending, 2020-2025

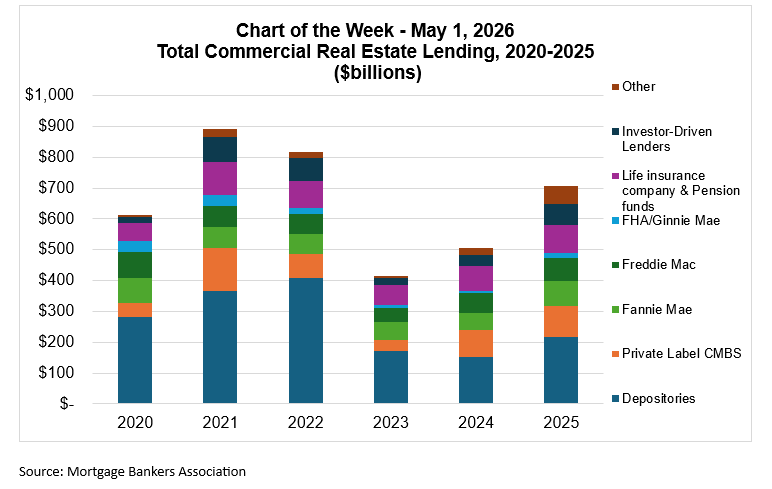

Based on the Mortgage Bankers Association’s (MBA) 2025 Commercial/Multifamily Annual Origination Volume Summation report, the commercial real estate lending market demonstrated meaningful recovery in 2025, with total origination volume reaching approximately $706 billion. This was a notable 40% increase over 2024’s $505 billion and significantly outpaced the market low experienced in 2023. While 2025 volume has not yet returned to the peak levels seen in 2021 or 2022, the rebound in 2025 signals renewed lender confidence and improving market conditions across most capital source categories.

Among the key lender segments, depositories led all capital sources in 2025, rebounding sharply from the prior year and recovering toward the elevated levels seen during 2021–2022. Agency lenders also showed strong momentum, with both Fannie Mae and Freddie Mac returning closer to their 2020 benchmarks after subdued activity in 2023 and 2024. Private label CMBS continued its upward trajectory, more than doubling its 2023 volume. Life insurance companies and pension funds held steady, while investor-driven lenders recovered meaningfully after a sharp pullback post-2022. FHA/Ginnie Mae volume also improved notably, climbing out of the suppressed range seen over the prior two years.

Overall, the 2025 data reflect a broad-based recovery across virtually every lender category. The most dramatic gains came from segments that were hardest hit during the 2023 contraction, suggesting that the market correction has largely run its course. While total volume remains approximately 21% below the 2021 cycle peak, the trajectory heading into 2026 is encouraging, particularly given the continued strength in agency and CMBS execution. Stakeholders should monitor whether depository and investor-driven lender activity can sustain current momentum as credit conditions and rate environments continue to evolve.

Reggie Booker (rbooker@mba.org)