Chart of the Week: New Residential Construction

Source: U.S. Census Bureau

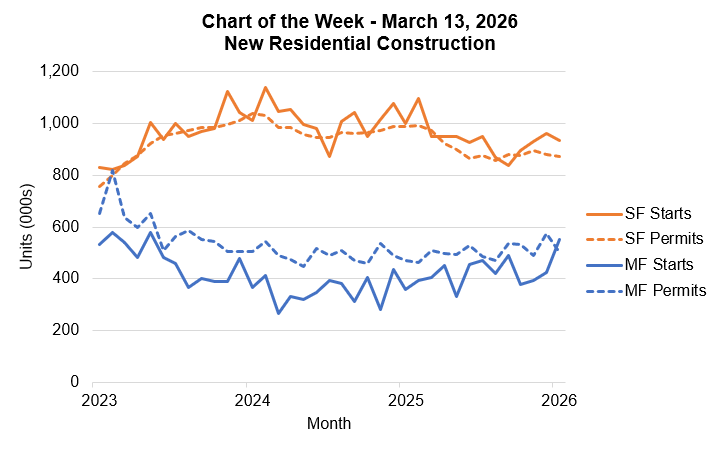

In 2025, single-family housing starts began at a relatively strong pace but gradually slowed over the year, bringing the average for 2025 to 943,000 units compared to 1.02 million in 2024. Single-family permits saw a similar decline in pace over the year, averaging just over 900,000 permits, compared to 980,000 permits in 2024. This decline in activity was due in part to slower demand as prospective buyers faced an uncertain economic and employment picture, and as affordability challenges lingered in certain markets. Builders also faced higher costs for inputs such as labor and materials, as well as permitting and regulatory hurdles.

The January data on housing starts released last week showed a similar start to 2026, with a SAAR of 935,000 single-family starts and 873,000 permits. Given the elevated level of unsold inventory for newly built homes as of December 2025–472,000 units, equivalent to an 8-month supply–we expect the tepid pace of single-family permitting and starts to continue through 2026. Homebuilders are likely to remain conservative about new starts and will continue to offer incentives to prospective homebuyers to sell their unsold inventory. Our forecast for single-family starts is for a relatively flat 2026 at around 930,000 units and for new home sales to increase relative to 2025’s levels, a SAAR of approximately 740,000 units, an 8% increase.

Multifamily (defined as 2+ units) permits and starts showed different trends, with both series growing in 2025 despite month-to-month volatility. Multifamily permits finished 2025 with a SAAR of 505,000 units, up from 495,000 units in 2024, and starts totaled 415,000 units, up significantly from 355,000 units in 2024. The January 2026 results showed that permits remained strong, despite declining from an elevated December level. Multifamily starts jumped to 552,000 units from 425,000, even as rents slowed and vacancy rates rose in many markets across the country, though the increase was driven by spikes in the South and Northeast. Our forecast is for multifamily starts to average around 390,000 units in 2026, though supply and demand will vary significantly across geographies. For example, some Sunbelt markets are seeing effective rents fall as vacancies increase, while vacancy rates remain tight in many East Coast metros.

Joel Kan (jkan@mba.org); Judith Ricks, Ph.D. (jricks@mba.org)