MBA Chart of the Week: 2023 HMDA Respondents

Source: 2019-2023 Home Mortgage Disclosure Act (HMDA)

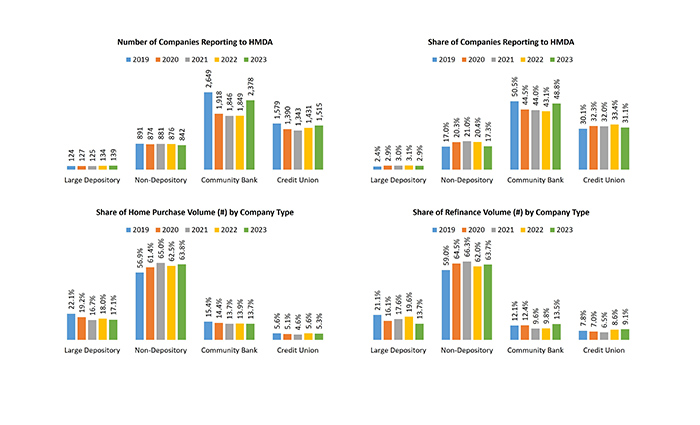

A total of 4,874 companies reported lending activity under the Home Mortgage Disclosure Act (HMDA) in 2023, according to MBA’s analyses of the dataset. This year’s jump in numbers was due to a drop in the loan-volume reporting threshold, from 100 closed-end loans (or 200 open-end lines of credit) originated in each of the preceding two calendar years for 2022, to 25 closed-end loans (or 200 open-end lines of credit) originated in each of the preceding two calendar years for 2023. Company types are defined by primary regulator and balance sheet assets, with large depositories holding assets of $10 billion or more.

Large depositories – historically, the smallest group of HMDA reporters – numbered 139 in 2023, their highest count since 2012. Given an increase in smaller depositories’ numbers due to the reporting threshold change, large depositories’ share of all HMDA reporters fell slightly to 2.9%. Though small in number, large depositories hold the second-largest market share, originating 17.1% of all home purchase loans and 13.7% of all refinance transactions in 2023. Large depositories lost their gains in market share from 2022, and their share of both the purchase and refinance market fell by more than any group last year – a drop of 0.9% for purchases and 5.9% for refinances. Their 13.7% refinance market share, specifically, was the lowest on record since 2008 (when MBA first started tracking this data).

Community banks – by contrast, the largest group – comprised over 90% of the increase in HMDA reporters and grew in number from 1,849 in 2022 to 2,378 in 2023. As a result, they were the only group to post an increase in their share of HMDA respondents, which was up 5.7% to 48.8% of all respondents. Despite this increase, community banks lost 0.2% share of the purchase market, likely because new community bank reporters were small lenders, originating just 25 or fewer loans in 2023. However, this was not the case for refinances, and community banks picked up more refinance market share than any other group and originated 13.5% of all refinance transactions last year.

Credit unions made up the rest of the increase in HMDA reporters and grew to 1,515 strong in 2023, making up 31.1% of HMDA reporters. Though second largest in number, the credit unions remain the smallest originators, holding just 4.8% of the purchase market and 7.5% of the refinance market on average since 2008. Credit unions lost 0.3% of their record-high 5.6% purchase market share in 2022 and ended 2023 originating 5.3% of all purchase loans. In contrast, they continued to see growth in the refinance market and originated 9.1% of these transactions in 2023, their highest share on record.

Non-depositories (IMBs), at 842 reporters, were the only group to see a decline in numbers in 2023. Representing less than one-fifth (17.3%) of HMDA respondents, the IMBs originated almost two-thirds (63.8%) of all loans last year. After losing market share for the first time in many years in 2022, the IMBs reversed course and posted gains in 2023. Their 1.3% gain in purchase market share fell short of their average annual gain of 2.5%; however, they still posted their second-best year on record and originated 63.8% of all purchase loans. Similarly, IMBs picked up a less-than-average 1.7% share of the refinance market and originated 63.7% of refinanced loans in 2023 – their third-highest share since 2008.

MBA’s HMDA data analyses are limited to the following: 1-4 unit, closed-end (or exempt), 1st lien loans originated through the retail/consumer direct, broker wholesale, or non-delegated correspondent channels. They exclude home improvement loans and loans with “other” or “not applicable” purposes. Though earlier iterations of the HMDA data are published by the CFPB in spring and early summer, MBA waits to publish its own analyses until mid-summer, after scrubbing the dataset of errors and outliers and allowing reporters time to correct and resubmit their data.

Please visit MBA’s HMDA webpage to view our suite of standard HMDA reports and explore custom reporting options. Our HMDA Residential Originations Databook (with 2023 data) is currently available for purchase and our HMDA Executive Databook is FREE for MBA members.

-Jon Penniman (jpenniman@mba.org)