MBA: IMBs Post Net Production Profit for First Time in Two Years

(Illustration credit: MBA)

Independent mortgage banks and mortgage subsidiaries of chartered banks reported a pre-tax net profit of $693 on each loan they originated in the second quarter, an increase from the reported loss of $645 per loan in the first quarter, according to the Mortgage Bankers Association’s new Quarterly Mortgage Bankers Performance Report.

“Net production income was positive in the second quarter of 2024–a welcome sign after eight consecutive quarters of net production losses,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “With a pickup in quarterly volume, productivity, and closings-to-applications pull-through, production costs dropped by about $1,800 per loan. These developments contributed to better net results, even as production revenues decreased from the previous quarter.”

Added Walsh, “Almost 80 percent of mortgage companies in the sample posted overall profits, including both production and servicing business lines. After two of the most challenging years in the mortgage business, many companies are seeing light at the end of the tunnel.”

Key findings of MBA’s Second-Quarter 2024 Quarterly Mortgage Bankers Performance Report include:

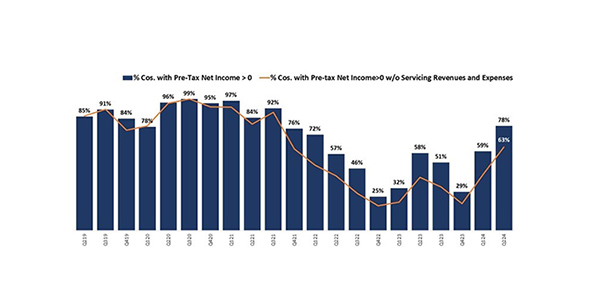

Including all business lines (both production and servicing), 78 percent of the firms in the report posted pre-tax net financial profits in the second quarter of 2024, up from 59 percent in the first quarter of 2024.

The average pre-tax production profit was 17 basis points (bps) in the second quarter of 2024, compared to an average net production loss of 25 bps in the first quarter of 2024, and a loss of 18 basis points one year ago. The average quarterly pre-tax production profit, from the third quarter of 2008 to the most recent quarter, is 42 basis points.

The average production volume was $492 million per company in the second quarter, up from $384 million per company in the first quarter. The volume by count per company averaged 1,503 loans in the second quarter, up from 1,193 loans in the first quarter.

Total production revenue (fee income, net secondary marketing income and warehouse spread) decreased to 347 bps in the second quarter, down from 371 bps in the first quarter. Average quarterly production revenue, from the third quarter of 2008 to the most recent quarter, is 347 basis points. On a per-loan basis, production revenues decreased to $11,499 per loan in the second quarter, down from $11,947 per loan in the first quarter.

The purchase share of total originations, by dollar volume, was 86 percent. For the mortgage industry as a whole, MBA estimates the purchase share was at 78 percent in the second quarter of 2024.

The average loan balance for first mortgages increased to $356,993 in the second quarter, up from $345,761 in the first quarter.

Total loan production expenses – commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations – decreased to 330 basis points in the second quarter of 2024 from 395 basis points in the first quarter of 2024. Per-loan costs decreased to $10,806 per loan in the second quarter, down from $12,593 per loan in the first quarter of 2024. From the second quarter of 2008 to last quarter, loan production expenses have averaged $7,524 per loan.

Servicing net financial income for the second quarter (without annualizing) was $69 per loan, down from $82 per loan in the first quarter. Servicing operating income, which excludes MSR amortization, gains/loss in the valuation of servicing rights net of hedging gains/losses, and gains/losses on the bulk sale of MSRs, was $88 per loan in the second quarter, down from $93 per loan in the first quarter.

MBA’s Mortgage Bankers Performance Report series offers a variety of other performance measures on the mortgage banking industry including revenue and cost breakouts, productivity, product mixes for originations and servicing volume, and pull-through rates. MBA’s Mortgage Bankers Performance Report is intended as a financial and operational benchmark for independent mortgage companies, bank subsidiaries and other non-depository institutions. Eighty-two percent of the 345 companies that reported production data for the second quarter of 2024 were independent mortgage companies, and the remaining 18 percent were subsidiaries and other non-depository institutions.

There are five Mortgage Bankers Performance Report publications per year: four quarterly reports and one annual report. Media wishing to view a copy of either report should contact Falen Taylor at (202) 557-2771 or ftaylor@mba.org. To purchase or subscribe to the publications, call (202) 557-2879. The reports can also be purchased on MBA’s website by visiting www.mba.org/PerformanceReport.