Mortgage Locks See Modest Rise in May, But Remain Suppressed, Black Knight Reports

(Courtesy Black Knight, Jacksonville, Fla.)

Mortgage lending improved in May compared to April, but remains constrained to say the least, reported Black Knight, Jacksonville, Fla.

Black Knight Vice President of Enterprise Research and Strategy Andy Walden said rate locks on purchase loans rose from April but noted they dipped to their lowest level yet relative to 2018/2019 averages as rates rose late in the month. “Mind you, purchase loans have been making up the lion’s share of origination activity for much of the last year, making this a likely harbinger of both slowing home sales as well as purchase mortgage origination volumes on the horizon,” he said.

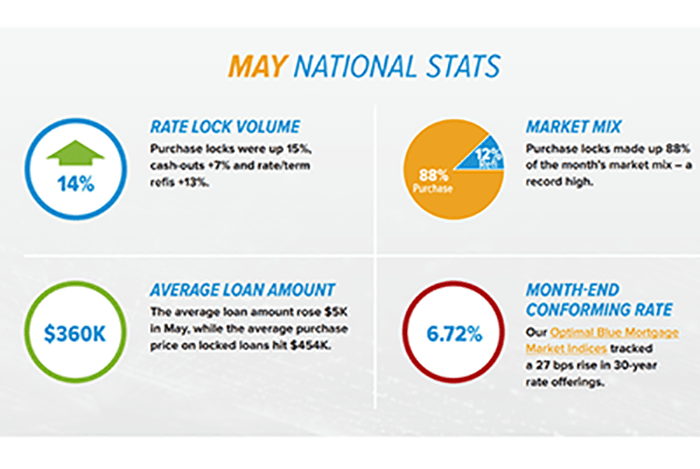

The month’s pipeline data showed locks increased 14% overall on a month-to-month basis, with purchase locks up almost 15%, cash-out refinances rising 7% and rate/term refinance locks climbing 13%. “The bulk of that increase can be attributed to May having two more business days than April,” Black Knight said in its Originations Mortgage Monitor report. “Adjusting for that, daily volume was up a more modest 4% month over month.”

Purchase locks accounted for 88% of locks in May, the highest share on record, Black Knight said. But even so, purchase lock counts were down 37% year-over-year and down 29% compared with pre-pandemic levels.

“Despite the many headwinds – and we all know them well by now: rates, affordability, prices and inventory – this remains the most purchase-dominant market we’ve seen in decades,” Walden said. “Nearly nine out of every 10 mortgages originated today is a purchase loan. At the same time, the level of economic uncertainty in the market has resulted in historically wide spreads between 10-year Treasury yields and 30-year mortgage rates, and that uncertainty seems to be trickling down to tightening credit standards across the board. Uncertainty breeds a fear of risk, and that is likely driving the rises we’ve seen in down payments and credit scores among recent originations. The credit box is certainly tightening, but it’s far from the only challenge facing prospective homebuyers.”