MBA Chart of the Week: FHFA Purchase Only House Price Index; MBA Forecast

Source: Federal Housing Finance Agency, MBA Forecast

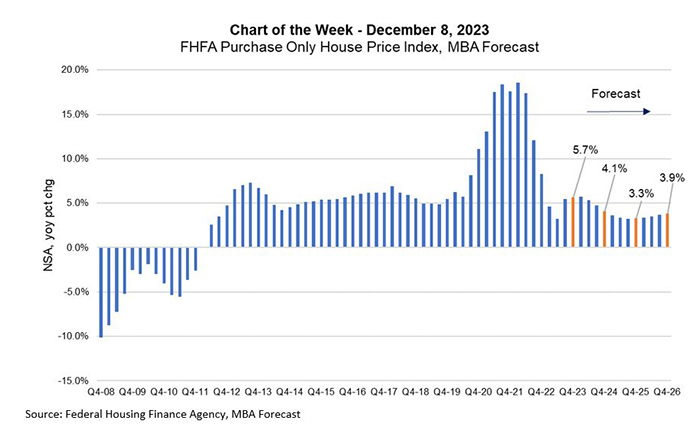

Home price appreciation across many parts of the country remains strong, despite low levels of home sales and potential buyers still waiting in the wings for mortgage rates to decline further. The Federal Housing Finance Agency’s house price index report for the third quarter of 2023 showed that aggregate home price appreciation over the 12-month period was 5.5 percent, continuing a streak of positive annual growth dating back to 2012.

Additionally, home prices increased in 49 states in the third quarter. This week’s Chart of the Week shows the historical national home price growth and MBA’s forecast through 2026. In MBA’s November forecast, we revised our home price appreciation path higher, given the stronger-than-expected third quarter reading driven by the ongoing lack of for-sale housing inventory. The bar chart highlights the fourth-quarter growth rates for 2023 to 2026, which are indicated in orange.

The National Association of Realtors reported that the inventory of existing homes on the market was 1.15 million in October, down almost 6 percent from a year ago. Between 2013 and 2020, this number averaged just under 2 million units. However, the inventory of newly built homes stood at 439,000 units in October 2023, based on data from the U.S. Census Bureau. This was lower than October 2022’s level of 460,000 units but above the 2013 to 2020 average of around 250,000 units.

Many existing homeowners are locked into lower mortgage rates, making them less willing to list and sell their homes, keeping inventory off the market. Potential buyers have turned to newly built homes as another option, and home builders have been able to meet this demand by increasing production and offering rate buydowns and other concessions to offset the impact of higher mortgage rates. Our forecast is for mortgage rates to decline over the next two years, decreasing from over 7 percent currently to the low 6-percent range by the end of 2024 and falling to under 6 percent in 2025. While mortgage rates are not expected to be as low as they were in recent years, lower rates will free up some for-sale inventory and exert downward pressure on home prices. The higher path for the home price forecast was accompanied by higher purchase origination dollar volume, as average loan sizes are expected to be larger.