Share of Mortgage Loans in Forbearance Falls to 0.85%

Mortgage loans in forbearance fell to new post-pandemic lows in May, the Mortgage Bankers Association reported Tuesday.

The MBA monthly Loan Monitoring Survey reported loans now in forbearance decreased by 9 basis points to 0.85% of servicers’ portfolio volume as of May 31 from 0.94% in April. MBA estimates just 425,000 homeowners remain in forbearance plans.

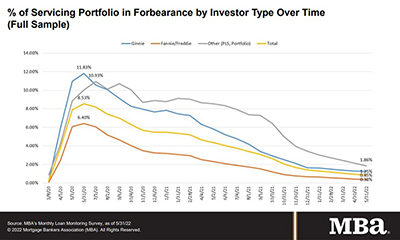

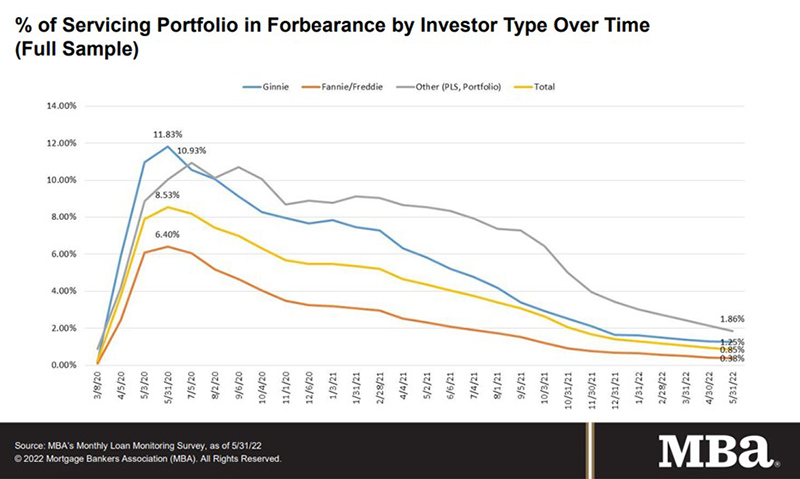

The share of Fannie Mae and Freddie Mac loans in forbearance decreased by 5 basis points to 0.38%. Ginnie Mae loans in forbearance decreased by 4 basis points to 1.25%, while the forbearance share for portfolio loans and private-label securities declined by 29 basis points to 1.86%.

“Servicers are whittling away at the remaining loans in forbearance, even as the pace of monthly forbearance exits slowed in May to a new survey low,” said Marina Walsh, CMB, MBA Vice President of Industry Analysis. “Most borrowers exiting forbearance are moving into either a loan modification, payment deferral or a combination of the two workout options.”

Walsh noted the overall servicing portfolio performance reached 95.85 percent current in May – 21 basis points higher than April’s figures. “However, it is worth watching if the rapid increase in interest rates for all loans, combined with inflation that is outpacing wage growth, complicates post-forbearance workout options and puts additional pressure on borrowers in existing post-forbearance workouts,” she said.

Key findings of MBA’s Loan Monitoring Survey – May 1 – 31

• Total loans in forbearance decreased by 9 basis points in May, from 0.94% to 0.85%.

o By investor type, the share of Ginnie Mae loans in forbearance decreased from 1.29% to 1.25%.

o The share of Fannie Mae and Freddie Mac loans in forbearance decreased from 0.43% to 0.38%.

o The share of other loans (e.g., portfolio and PLS loans) in forbearance decreased from 2.15% to 1.86%.

• Loans in forbearance as a share of servicing portfolio volume (#) as of May 31:

o Total: 0.85% (previous month: 0.94%)

o Independent Mortgage Banks (IMBs): 1.06% (previous month: 1.17%)

o Depositories: 0.67% (previous month: 0.74%)

• By stage, 28.2% of total loans in forbearance are in the initial forbearance plan stage, while 58.6% are in a forbearance extension. The remaining 13.2% are forbearance re-entries, including re-entries with extensions.

• Of the cumulative forbearance exits for the period from June 1, 2020, through May 31, 2022, at the time of forbearance exit:

o 29.4% resulted in a loan deferral/partial claim.

o 18.7% represented borrowers who continued to make their monthly payments during their forbearance period.

o 17.1% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

o 15.7% resulted in a loan modification or trial loan modification.

o 11.2% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

o 6.7% resulted in loans paid off through either a refinance or by selling the home.

o The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

• Total loans serviced that were current (not delinquent or in foreclosure) as a percent of servicing portfolio volume (#) rose to 95.85% in May from 95.64% in April (on a non-seasonally adjusted basis).

o States with the highest share of loans that were current as a percent of servicing portfolio: Idaho, Washington, Colorado, Utah and Oregon.

o States with the lowest share of loans that were current as a percent of servicing portfolio: Mississippi, Louisiana, New York, West Virginia and Illinois.

• Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts declined to 82.75% last month from 82.99% in April.

MBA’s monthly Loan Monitoring Survey (replaced MBA’s Weekly Forbearance and Call Volume Survey in

November 2021) represents 70% of the first-mortgage servicing market (36.0 million loans).

To subscribe to the full report, go to www.mba.org/loanmonitoring.