Purchase Applications Up, Overall Applications Down As Rates Hit Record Low in MBA Weekly Survey

Mortgage applications fell again last week despite an uptick in purchase applications and even as the 30-year fixed mortgage rate dropped to a record low, the Mortgage Bankers Association reported in its Weekly Mortgage Applications Survey for the week ending April 24.

The Market Composite Index decreased by 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased by 2 percent compared to the previous week.

The unadjusted Refinance Index decreased by 7 percent from the previous week and was 218 percent higher than the same week one year ago. The refinance share of mortgage activity decreased to 71.6 percent of total applications from 75.4 percent the previous week.

The seasonally adjusted Purchase Index increased by 12 percent from one week earlier. The unadjusted Purchase Index increased by 13 percent compared to the previous week and was 20 percent lower than the same week one year ago.

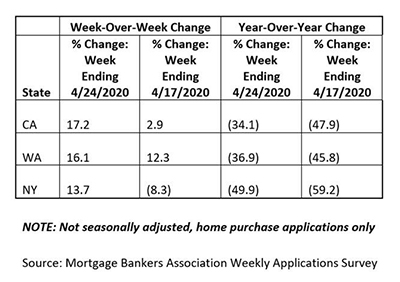

Looking at the impact at the state level, here are results showing the non-seasonally adjusted, week over week percent change in the number of purchase applications from Washington, California and New York:

The FHA share of total applications increased to 11.5 percent from 10.3 percent the week prior. The VA share of total applications decreased to 13.3 percent from 13.8 percent the week prior. The USDA share of total applications increased to 0.5 percent from 0.4 percent the week prior.

“The news in this week’s release is that purchase applications, still recovering from a five-year low, increased 12 percent last week to the strongest level in almost a month,” said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. “The 10 largest states had increases in purchase activity, which is potentially a sign of the start of an upturn in the pandemic-delayed spring home buying season, as coronavirus lockdown restrictions slowly ease in various markets. California and Washington continued to show increases in purchase activity, with New York seeing a significant gain after declines in five of the last six weeks.”

Kan noted contributing to the uptick in purchase applications was that mortgage rates fell to another record low in MBA’s survey, with the 30-year fixed rate decreasing to 3.43 percent. “However, refinance activity declined 7 percent, as rates for refinances likely remained higher than those for purchase loans,” he said. “Lenders are still working through pipelines at capacity, and observed changes in credit availability for refinance loans have also in turn impacted rates.”

MBA reported the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($510,400 or less) decreased to 3.43 percent from 3.45 percent, with points increasing to 0.34 from 0.29 (including origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $510,400) decreased to 3.72 percent from 3.81 percent, with points decreasing to 0.33 from 0.34 (including origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by FHA increased to 3.39 percent from 3.33 percent, with points increasing to 0.20 from 0.19 (including origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 2.98 percent from 3.03 percent, with points decreasing to 0.28 from 0.33 (including origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 5/1 adjustable-rate mortgages remained unchanged at 3.29 percent, with points increasing to 0 from -0.15 (including origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The ARM share of activity increased to 2.9 percent of total applications.

The survey covers more than 75 percent of all U.S. retail and consumer direct residential mortgage applications and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks and thrifts.