Mark P. Dangelo: Are Bankers Necessary? Part 2

(Mark P. Dangelo is president of MPD Organizations LLC, featuring books, industry reports and articles. He is a strategic management consultant, outsourcing advisor and analytics specialist with extensive process, technology and financial results and is a frequent contributor to MBA NewsLink. He can be reached at mark@mpdangelo.com or at 440/725-9402.)

It has been expressed, “we are humans and we are incredibly clever.” During times of great consternation and uncertainty brought on by COVID-19, let us hope we live up to both. Prayers and empathy go out to those afflicted, and apologies in advance for the continuation of our discussion during times of unprecedented turmoil.

Yet, as consumers, politicians, healthcare, financial services and banking organization, educators and counseling workers struggle with the “next normal”, what is now striking is the speed and functionality for social distancing and lockdowns impacting daily lives—not to mention rising fatalities. For many years, the organizational and individual resistance to adaptation for remote work, distance collaboration, and even education and reskilling, were billed as one-offs and impractical. However, in a period of weeks, forced by an invisible virus, our business polices, practices, methods, attitudes have been shattered allowing for an embrace (albeit reluctantly) of the once discounted.

Yes, we have a long way to go to provide demographic and economic delivery of features and consistently applied equality across education, high-bandwidth and 5G, individual security and privacy just to mention a few necessities exposed during this time of crisis management.

Yes, Pandora has been released and the implications that arise will create unworkable business models not only for existing and well-funded FSBOs, but also start-ups and future entrepreneurs seeking to make their mark in the world.

Yes, we are just now understanding that the unprecedented support of consumers thrown out of work and government intervention to stem potential defaults and missed payments, will lead to a vast array of unintended consequences for traditional banks, non-bank lenders, fintech startups and even large retailers who had hoped to transfer financial market functions into their domains.

And yes, management styles and remote worker productivity will all have to evolve, change, and adapt—regardless of the spyware introduced by FSBOs on their employees and their home computers.

While COVID-19 may provide a brief internal reprieve for a robust discussion of “Are Bankers Necessary?”, these unprecedented events lay the arguments and groundwork for a vast number of “next normal” potentials. Pandora has been released into the FSBO world—so what will be afflicted? Will the living wills be tapped as institution draw down credit lines and routinely access the Federal Reserve windows? Will the rescue funds for FSBO’s replenished over the last decade be once again necessary?

More importantly, if tapped and markets consolidate, will this be another decade of radical change coming after a Golden Age of growth and historic profitability? As the pandemic unfolds, governments rush to react, and the impacts fueled by those unintended consequences rise, will the positions and risks taken by banks and non-banks usher in a comprehensive culling of institutions once thought to be safe, sound, and worthy of our trust?

Even before the reality of pandemics, FSBOs were starting to feel the strain of business practices and leverage. This is where we started in early March.

The numbers confronting FSBOs before the pandemic crisis were not optimistic. The profits reaped during times of prosperity were giving way to deep concerns of longer-term benefits and industry consolidation. As assets became concentrated and consumers increasingly seeking FSBO alternatives that are easier to use, cheaper, and integrated to daily life (e.g., tied to integrated home voice assistants), the value-add of the banker beyond an order taker and an intermediary forced many startups and non-traditional competitors to answer with “bankers are not necessary.”

A Confluence of Factors

None of the strategy models or economic projections could have anticipated that 2020 would be the year which delivered comprehensive disruption that had little to do with advanced innovations. Additionally, the demographic markets that projected the rise of Millennials now has FSBOs transitioning to Gen Z to set the emerging standards for consumerism and behavioral models of the future. Now, with COVID-19 and the lasting repercussions, the use of rapidly expanding innovations that do not rely on humans or contact—AI, machine learning, data sciences, remote collaboration, RPA—will become the norm for process automation and consumer expansion in the face of human-to-human avoidance.

However, with many factors now in play, with operating and behavioral norms now sidelined, where will FSBOs turn to achieve instantaneous, social-distanced delivery? Will partners step up? Are employee skills up to the challenges? How many of the existing solutions and fintech providers will be able to withstand the tidal wave of factors impacting business models, fund raising, and risks? And, while some business and political leaders hope for a fast recovery from the pandemic (e.g., a “V” shaped bottom), where will reality take us, and more importantly, how many organizations have the crisis skills needed to react to and survive cascading waves of black-swan events? Will enterprises be able to hang on for what mainstream economists are now projecting to be a minimum of a three-quarter long recession?

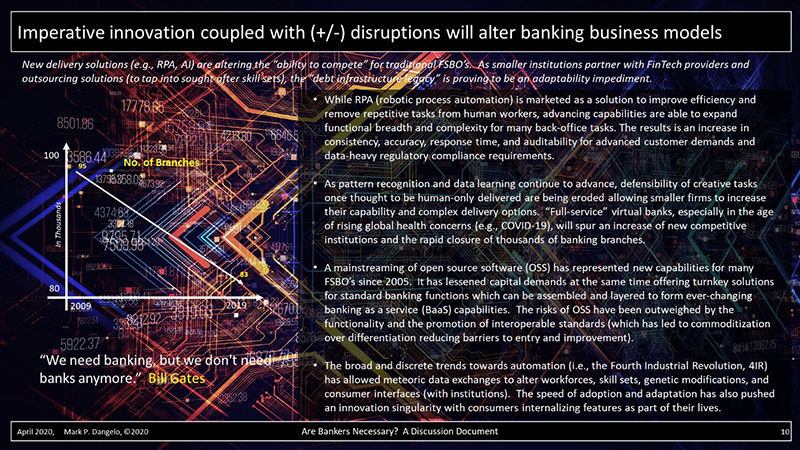

It was in the 1990s when Bill Gates stated, “We need banking, but we don’t need banks anymore.” The debate 25 years later still rages on—was he right or misguided? Since the 1990s a confluence of factors has materially changed every aspect of FSBOs from the back-office to customer experiences and now to BaaS (banking as a service).

And, while everyone is currently focused on the events and outcomes of the COVID 19 pandemic, the revealing of the fourth industrial revolution (4IR) has brought forth disruption—across every industry, business, and worker. As routine functions are automated (e.g., AI and robotics), new options will be available for those willing to adapt to changing demands and skill requirements (as the average half-life of an education will be less than four years by 2023).

The reactions to COVID-19 will lay the seeds for future growth. Whereas COVID-19 is a game changer, it will usher major disruptions that were already underway. Moreover, as FSBOs have shifted risks into unregulated areas, which if estimates are accurate, could bring exposures (e.g., swaps, CLOs, margin calls, credit-risk transfers) to more than $1 trillion.

As cascading events of pandemic unemployment expand, how many businesses and consumers will be delaying payments, drawing credit lines down, seeking forgiveness, or outright defaulting on covenants that until invoked, have unattributed risks that will accelerate the demise of many storied FSBOs? How many institutions have risks outside a regulator’s control that will once again become catalysts for a global financial reckoning? Will the fallout from the pandemics lead to another vilification of activities FSBOs were doing, which while meeting the “letter of the law” violated “the spirit of the law?” So, will it become the watershed movement for consumers to ask and answer “are bankers necessary?”

Key Imperatives and Transformative Unbundling

Banks in times of crisis typically become a key institution to calm markets and hold together a global financial system built on vast data, millisecond interchanges and an implicit trust that regardless of social and economic consequences the assets of a typical customer are protected under regulatory guidelines and watchful central bankers. However, in times of rapid economic collapse, vast sovereign debts (with many GDPs far less that government debt), and newly minted, historic stimulus programs, will the short-term reprieves become the death knells for “Are bankers necessary?”

Let’s step back from the COVID-19 reality, to the innovative transformations that were already in the pipelines before, and the potential impacts after this has reached its apex.

- AI will make decisions and rise to a sophistication well beyond trend analysis, dark-data mining, and as hacking toolsets. AI’s impact on pandemic mitigation will be unprecedented.

- AI will accelerate the capability and delivery of AR bringing customized for specialized work functions aiding for faster delivery and granular delivery.

- With standards and the deep discovery of data correlations, insights and predictions will become routine with more advanced capabilities moving from administrative into cognitive.

- Homes and their infrastructure will provide a flood of new sciences and disciplines expanding on the IoT explosions—intelligent buildings, VR and AR out-of-body experiences, pretesting for healthcare—while removing mundane tasks such as bill paying, grocery shopping, and home maintenance from consumer duties.

- Within homes and businesses, smart walls (e.g., Samsung Neon) will emerge blending together chatbot advancements with visually appealing consumer “synthetic beings” who act on the behalf of the occupant to conduct their lives, interact in conversational cadence, manage their affairs and resolve conflicts.

- As AI, VR and AR become synonymous with the individual who uses them, rising innovation singularity issues will advance, yet stretch, regulatory compliance and legal boundaries.

For FSBOs to compete in a virtual world and one that will likely accelerate the declining value of physical branches, the acceptance and partnering with market leaders and emerging enterprises will require orchestration efforts to unbundle and compartmentalize functions (and technology) to arrive at building blocks of financial functions. These unbundled building blocks can then be assembled, reassembled, and dismantled with clear inputs, outputs, and auditing of data with greater iteration capabilities—all needed during this time of pandemic responses.

Examples of the impacts of these emerging solutions and techniques coupled with disruptions already in play will lead many FSBO institutions to transform their operations over the next 12 months. For these leaders embracing the disruption, they will be driving the answer to the question, “are bankers necessary?”

Below is a panel of disruptions that are already occurring. With the pandemic gripping social and governmental attention, the next iterations of these disruptors are underway and the impacts for traditional FSBO’s already losing an average of 200 to 250 institutions every year for decades will be deep and pervasive. Is your organization anticipating what is next—or just trying to survive as interconnected crisis’s move across markets that just a month ago were near their peaks?

It has been said that after the storm comes the rainbow—but unlike determinists, I only look for better things if I have prepared for it. In Part 3, we will explore emerging options and alternatives to the traditional value-add bankers have claimed as part of their mandatory participation in the demand for banking.

In the meantime, like educators, workers, and even government leaders who were adamant that functions could not be delivered digitally, only to have proven that in crisis they could, what will bankers do when swaths of functionality once deemed value-added requiring their skills become streamlined, automated, and further commoditized? Like Pandora who when the box was opened was repeatedly bitten by moths representing human afflictions, it would seem realistic that bankers need to start asking before recovery, “Are Bankers Necessary?” Otherwise, perhaps they should purchase vast quantities of soothing lotions in advance and sell them on the open markets?

(Views expressed in this article do not necessarily reflect policy of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes your submissions. Inquiries can be sent to Mike Sorohan, editor, at msorohan@mba.org; or Michael Tucker, editorial manager, at mtucker@mba.org.)