“Banks have a very small sandbox with which to play, and they have to either have something on hand, or something to get rid of. Banks will probably need to hold on to more liquid assets in the future, and mortgages will probably become more attractive than Treasuries. Over the next year, I expect an asset build.”

–Nicholas Maciunas, Executive Director with JPMorgan Chase, New York.

Category: News and Trends

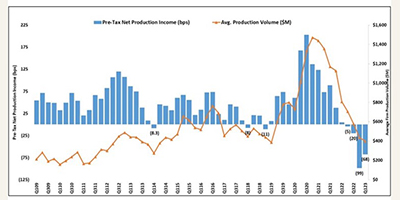

MBA: IMBs Report Pre-Tax Net Production Losses in 1Q

Independent mortgage banks and mortgage subsidiaries of chartered banks reported a net loss of $1,972 on each loan they originated in the first quarter, an improvement from the reported loss of $2,812 per loan in the fourth quarter, the Mortgage Bankers Association reported Thursday.

Terrell Cassada of LoanLogics: Real Secondary Market Loan Confidence Happens from Within

New technologies, including AI, machine learning tools and rules-driven workflow, are finally being applied to the loan production process with gusto. Real results are being achieved through automation that drives fewer underwriting touches and exposes quality issues earlier in the production process. And now the secondary market—one of the last remaining components of loan manufacturing still awash in spreadsheets, manual processes, and data inconsistencies—is finally getting its turn at bat.

Seth Sprague, CMB, of Richey May: Now’s the Time to Prepare for FHFA/Ginnie Mae Rules Changes for Non-Bank Servicers

On August 17, 2022, the Federal Housing Finance Agency and Ginnie Mae jointly announced updated minimum financial eligibility and capital rules for seller/servicers and issuers. These changes update the capital and financial eligibility requirements for non-bank servicers that have been modified over the past year. Understanding the new requirements is critical for seller/servicers and issuers to maintain compliance; however, these changes also raise potential strategic and operational challenges in the future.

Elevating Your Quality Quotient, Part II: Mortgage Servicing Post-Pandemic

Regulations offer guardrails, but rebuilding trust is key to a vibrant mortgage servicing industry. The hurdles of the Great Financial Crisis have been largely overcome and the COVID-19 Pandemic National Emergency was formally decreed behind us on April 10. So, what does the marketplace for servicing look like today and what aspects of servicing could look different in the future?

#MBASecondary23: Broeksmit: ‘You Don’t Need Punishment or More Regulation; You Need Praise and Relief—and You Need it Now’

NEW YORK—When Mortgage Bankers Association President & CEO Bob Broeksmit, CMB, stepped on stage Monday here at the National Secondary Market Conference & Expo, he promised a presentation “more pugnacious than normal.” And he delivered.

#MBASecondary23: The Future of Financial Stability

NEW YORK—What issues are affecting the financial markets? Here at the Mortgage Bankers Association’s National Secondary Market Conference & Expo, panelists said much of the future depends on what happens—or doesn’t happen—in Washington, D.C. over the next year or so.

Sponsored Content from SWBC: Mortgage Market Outlook and Risk Management Strategies for Lenders

As the mortgage market continues to evolve, mortgage servicers face new challenges and opportunities. A solid understanding of the latest industry trends, economic outlook, and regulatory requirements is essential for success in this competitive landscape.

Terrell Cassada of LoanLogics: Real Secondary Market Loan Confidence Happens from Within

New technologies, including AI, machine learning tools and rules-driven workflow, are finally being applied to the loan production process with gusto. Real results are being achieved through automation that drives fewer underwriting touches and exposes quality issues earlier in the production process. And now the secondary market—one of the last remaining components of loan manufacturing still awash in spreadsheets, manual processes, and data inconsistencies—is finally getting its turn at bat.

Elevating Your Quality Quotient, Part II: Mortgage Servicing Post-Pandemic

Regulations offer guardrails, but rebuilding trust is key to a vibrant mortgage servicing industry. The hurdles of the Great Financial Crisis have been largely overcome and the COVID-19 Pandemic National Emergency was formally decreed behind us on April 10. So, what does the marketplace for servicing look like today and what aspects of servicing could look different in the future?