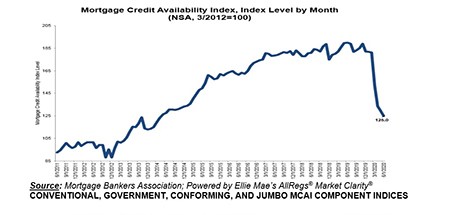

Mortgage credit availability fell in June for the fourth consecutive month, remaining at a six-year low, the Mortgage Bankers Association reported this morning.

Category: News and Trends

Housing Finance Market Roundup

Here’s a summary of recent reports about the housing market and real estate finance, with reports from Zillow; Veros Real Estate Solutions; Fannie Mae; Redfin; Genworth Mortgage Insurance; and Computershare Loan Services.

Fitch Ratings: Coronavirus Sparks Largest-Ever CMBS Delinquencies Rate Jump

June saw the largest month-over-month increase in the commercial mortgage-backed securities delinquency rate in more than 15 years, reported Fitch Ratings, New York.

Faith Schwartz: New Era Borne of Pandemic to Upend Mortgage Costs

As longtime industry participants, we at Housing Finance Strategies contend that the pandemic has created a revolutionary opportunity that we must seize and leverage so that the mortgage business can emerge with higher quality prospective products funded through a drastically reduced cost structure.

Dealmaker: Newmark Knight Frank Arranges $55M Office Portfolio Sale

Newmark Knight Frank, New York, brokered $55 million for a suburban office portfolio in Westlake Village, Calif.

Andrew Foster: Preferred Equity Plan for Commercial Real Estate Comes to Washington

This week in Washington, ongoing COVID-19 relief discussions have reached the commercial real estate borrowing community and their financiers in earnest.

Mortgage Applications Increase in MBA Weekly Survey

Mortgage applications increased for the first time in three weeks as key mortgage rates fell to yet another record low, the Mortgage Bankers Association reported this morning in its Weekly Mortgage Applications Survey for the week ending July 3.

Fannie Mae: Explore eClosing Scenarios

Did you know electronic closings can occur in different ways? Take a closer look at two digital closing scenarios: hybrid and full eClosing with remote online notarization (RON).

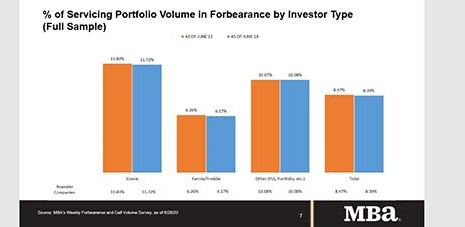

MBA: Share of Mortgage Loans in Forbearance Decreases for Third Straight Week to 8.39%

The Mortgage Bankers Association’s latest Forbearance and Call Volume Survey reported loans now in forbearance decreased by 8 basis points to 8.39% of servicers’ portfolio volume as of June 28, compared to 8.47% the prior week. MBA estimates nearly 4.2 million homeowners are in forbearance plans.

Michael Steer & Erin Harris: Accelerated Digital Mortgage Tech Strategies Must Also Include Sound Vendor Management

Adherence to vendor management best practices needs to remain top of mind for lenders even when accelerating their digital mortgage tech selection and deployment process. Compliance with regulatory requirements and proper risk mitigation are not steps to be overlooked.