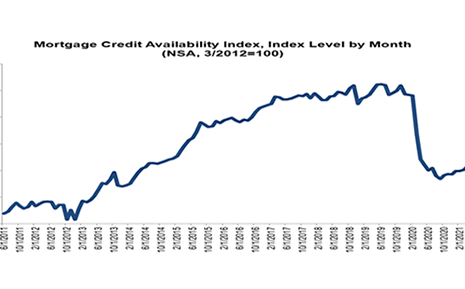

Mortgage credit availability increased slightly in July after a big drop in June, the Mortgage Bankers Association reported Thursday.

Category: News and Trends

MBA Opens Doors Foundation Welcomes Lennar Mortgage’s Laura Escobar to Board of Directors

The MBA Opens Doors Foundation welcomed Lennar Mortgage President Laura Escobar to its Board of Directors.

MBA Recognizes Select Members

MBA is proud to recognize its Premier and Select Associate Members and to thank them for their continued support of MBA and the real estate finance industry.

MBA: Second Quarter Commercial/Multifamily Borrowing Bounces Back

Commercial and multifamily mortgage loan originations jumped by 106 percent in the second quarter from a year ago and increased by 66 percent from the first quarter, according to the Mortgage Bankers Association’s Quarterly Survey of Commercial/Multifamily Mortgage Bankers Originations.

MBA Recognizes Premier Members

MBA is proud to recognize its Premier and Select Associate Members and to thank them for their continued support of MBA and the real estate finance industry.

MBA DEI Leadership Awards: Nomination Deadline TODAY

Inspire change; share success. The Mortgage Bankers Association recognizes residential and commercial/multifamily members who show leadership in the areas of Diversity, Equity and Inclusion (DEI) internally through market outreach efforts with its annual DEI Leadership Awards.

Andrew Foster: Multifamily Values Amid a Shifting Landscape

The summer has brought big news for the housing industry including but not limited to multifamily market participants.

July Mortgage Credit Availability Increases Slightly

Mortgage credit availability increased slightly in July after a big drop in June, the Mortgage Bankers Association reported Thursday.

ICE: Purchases Eclipse Refinances for First Time in 18 Months

ICE Mortgage Technology, Pleasanton, Calif., reported new home purchases represented a higher percentage than refinances for the first time in nearly two years.

MBA: Second Quarter Commercial/Multifamily Borrowing Bounces Back

Commercial and multifamily mortgage loan originations jumped by 106 percent in the second quarter from a year ago and increased by 66 percent from the first quarter, according to the Mortgage Bankers Association’s Quarterly Survey of Commercial/Multifamily Mortgage Bankers Originations.