Fitch Ratings: U.S. Life Insurers’ Commercial Mortgages Stable Amid Growing Headwinds

Fitch Ratings, New York, said U.S. life insurers’ commercial mortgage fundamentals have largely recovered since the pandemic, with stable property outlooks for hotel, office retail and multifamily sectors.

However, Fitch cautioned the Federal Reserve’s monetary tightening and current conditions could pressure some sectors of commercial mortgages over the midterm, with consistently high inflation and rising interest rates negatively affecting some property valuations.

Fitch reported U.S. life issuers allocated 13% of their total investment portfolios to mortgages in 2021, in line with 2020 but above historical levels of 8%–12%.

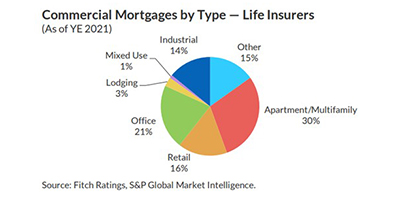

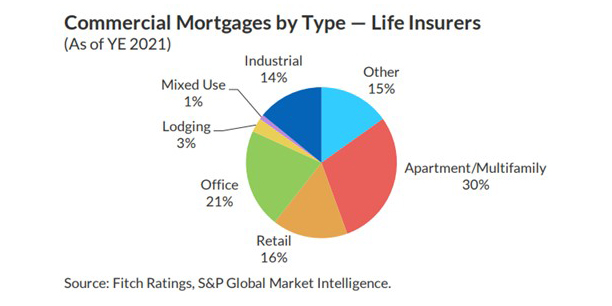

“This above-average concentration could leave investment portfolios potentially more vulnerable in a declining real estate scenario,” said Laura Kaster, Senior Director with Fitch Wire. “However, life insurers have moderate exposure to retail and office properties and limited exposure to hotel, the sectors expected to be the most affected from an economic slowdown and elevated inflation pressures.”

Fitch said given rising rates, insurer mortgage growth is expected to moderate and focus on high quality investments to manage risk. The level of higher quality loans stabilized after slight declines prior to the pandemic, with 53% of mortgage loans at the CM1 level, or the strongest quality.

Life insurers also maintained favorable loan-to-value ratios of 53.5% in the first half of 2022, down from 55.1% in 2021, 55.3% in 2020 and 58.0% in 2019. Fitch said conservative LTVs are expected to remain at current levels over the near term, which should help life insurers manage investment risks in a weaker economy with slowing demand.

Fitch reported U.S. commercial mortgage-backed securities loan delinquencies fell to 2.1% as of June, down from a peak of 5.0% in July 2020. Fitch expects CMBS delinquencies to decline to 1.25% by year-end 2022, based on healthy new issuance volume, improved resolution volume outpacing defaults and an increased number of maturing loans able to refinance versus the prior two years.

“However, uncertainty is growing around the effects of inflation and rising rates on resolution velocity, new issuance volume and property valuations,” Fitch said.