Milliman, Seattle, said its Milliman Mortgage Default Index shows a slight increase in the lifetime serious delinquency rate (for homes 180-plus days delinquent) for U.S.-backed mortgages.

Tag: Jonathan Glowacki

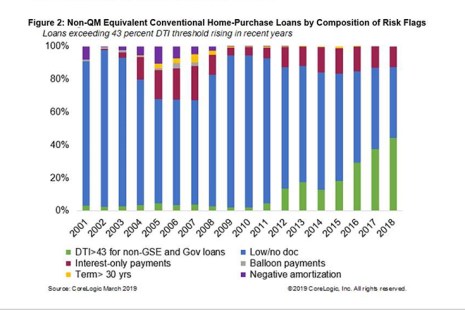

Portfolio Risk Management: Repurchase Risk for Non-QM Mortgages

In the wake of the 2008 global financial crisis, many risk managers in the mortgage issuance industry were caught flat-footed with representations and warranties exposure, also commonly known as repurchase exposure. R&W agreements often require the issuer of mortgages to repurchase the loans and make whole the investors if the loans are found to breach the seller guidelines.