MBA: Mortgage Delinquencies Increase in the Fourth Quarter

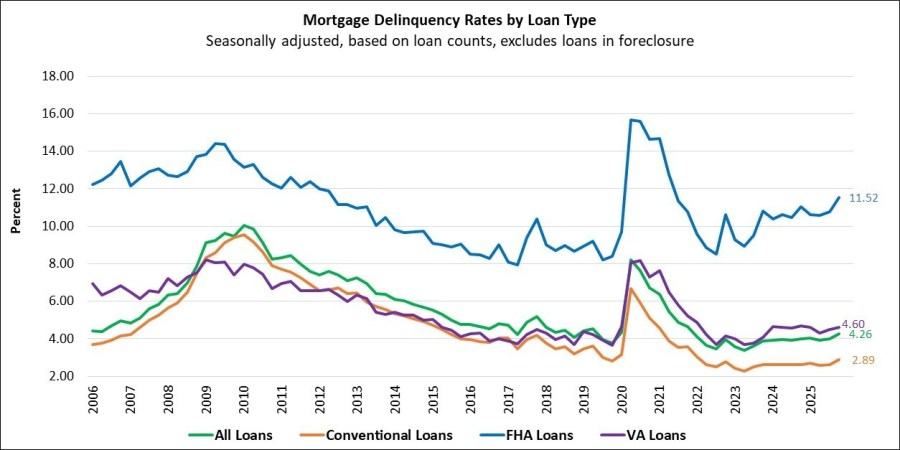

The delinquency rate for mortgage loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 4.26% of all loans outstanding at the end of the fourth quarter of 2025, according to the Mortgage Bankers Association’s National Delinquency Survey.

The delinquency rate was up 27 basis points from the third quarter of 2025 and up 28 basis points from one year ago. The%age of loans on which foreclosure actions were started in the fourth quarter remained unchanged at 0.20%.

“Mortgage delinquencies increased across all three major loan types – Conventional, FHA, and VA – in the last three months of the year,” said Marina Walsh, CMB, MBA’s vice president of industry analysis. “The most pronounced uptick was with FHA loans, which reached a delinquency rate of 11.52%, the highest level since the second quarter of 2021. While earlier-stage FHA delinquencies remained relatively flat compared to the previous quarter, later-stage, 90+ day delinquencies increased by 76 basis points. The FHA foreclosure inventory rate also grew to the highest level since the first quarter of 2020.”

Added Walsh, “The fourth quarter results may have been impacted by the expiration of pandemic-era, FHA relief options as well as disparities in the labor market – a key determinant of mortgage delinquency levels.”

Walsh noted that serious delinquencies – which include loans 90+ days delinquent and in foreclosure – vary by year of origination. For FHA loans, the vintage years 2020 and 2021 are performing better than the vintage years 2022 and 2023, when mortgage rates rose and affordability was especially stretched. With FHA volume increasing, mortgage rates moderating, and borrower credit characteristics improving on newer FHA originations, the performance of recent cohorts may temper stress on overall FHA portfolios.

Key findings of MBA’s Fourth Quarter of 2025 National Delinquency Survey:

• Compared to last quarter, the seasonally adjusted mortgage delinquency rate increased for all loans outstanding. By stage, the 30-day delinquency rate decreased 5 basis points to 2.07%, the 60-day delinquency rate increased 16 basis points to 0.92%, and the 90-day delinquency bucket increased 16 basis points to 1.27%.

• By loan type, the total seasonally adjusted delinquency rate for conventional loans increased 27 basis points to 2.89% over the previous quarter. The total FHA seasonally adjusted delinquency rate increased 74 basis points to 11.52%, and the total VA seasonally adjusted delinquency rate increased 10 basis points to 4.60%.

• On a year-over-year basis, total mortgage delinquencies increased for all loans outstanding. The delinquency rate increased 27 basis points for conventional loans, increased 49 basis points for FHA loans and decreased 10 basis points for VA loans from the previous year.

• The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The%age of loans in the foreclosure process at the end of the fourth quarter was 0.53%, up 3 basis points from the third quarter of 2025 and 8 basis points higher than one year ago.

• The non-seasonally adjusted seriously delinquent rate, the%age of loans that are 90 days or more past due or in the process of foreclosure, was 1.85%. It increased 24 basis points from last quarter and increased 17 basis points from last year. The seriously delinquent rate increased 9 basis points for conventional loans, increased 106 basis points for FHA loans, and increased 28 basis points for VA loans from the previous quarter. Compared to a year ago, the seriously delinquent rate remained unchanged for conventional loans, increased 104 basis points for FHA loans and remained unchanged for VA loans.

• The five states with the largest quarterly increases in their overall delinquency rate were: Mississippi (109 basis points), Louisiana (89 basis points), Maryland (87 basis points), Oklahoma (86 basis points), and Indiana (86 basis points).

For the purposes of the survey, MBA asks servicers to report loans in forbearance as delinquent if the payment was not made based on the original terms of the mortgage.

NOTE: For non-seasonally-adjusted (NSA) supplemental information on the performance of servicing portfolios by investor type, loans in forbearance by investor type, and the status of post-forbearance workouts, as well as servicer call volume metrics, please refer to MBA’s Monthly Loan Monitoring Survey.