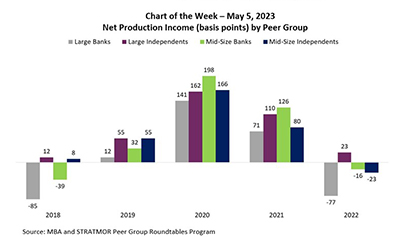

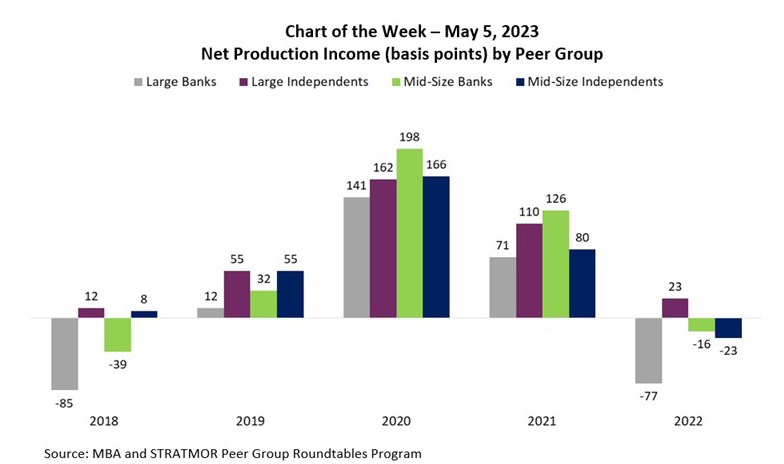

MBA Chart of the Week May 5, 2023: Net Production Income by Peer Group

MBA Research conducts a series of benchmarking programs focused on mortgage profitability, revenue, cost, product mix and productivity. Last month, we released results from our MBA Annual Performance Report and we regularly post data from our MBA Quarterly Performance Reports. These reports are representative of independent mortgage companies (IMBs) and a handful of bank subsidiaries that are Ginnie Mae issuers and/or Fannie/Freddie seller/servicers. But the question is often raised, “What about the banks – the mortgage lending divisions of a bank? How are they faring?”

In this week’s MBA Chart of the Week, we look at pre-tax net production income from a different source – the MBA and STRATMOR Peer Group Roundtables Program. This program was started in 1998 along with STRATMOR Group and is our most comprehensive data collection – providing results for both banks and independents, and then further divided by volume and business model.

Participating companies in this week’s chart are consolidated into four major peer groups. Volume thresholds differ from year-to-year, but the general threshold between large and mid-size is $5 billion, and almost all mid-size companies have more than $1 billion.

From 2018-2022, the cyclical nature of the mortgage business is on full display, with minimal to no profits in 2018 and 2022, and study-high profits in 2020. In the low-volume years of 2018 and 2022, banks posted net production losses while independents hovered closer to break-even. Combined, the net production income for all independent mortgage companies in the PGR sample averaged 1 basis point in 2022, compared to average losses of 37 basis points for banks.

These were not the only years that banks posted net production losses. How can that be? Unlike most IMBs, some banks can justify operating at a production loss because of the ongoing net interest margin generated on loans held for investment, ability to cross-sell other bank products, and having other business lines that are profit-generating when the mortgage originations division is not.

Notes:

- Pre-tax net production income in basis points is defined as total revenues (fee income, secondary marketing income, value of capitalized servicing/servicing released premiums and net warehouse spread) minus fully-loaded production costs (sales, fulfillment, production support and corporate costs), divided by production volume in dollars ($), multiplied by 10,000. Ongoing changes in the value of mortgage servicing rights after origination are excluded.

- For banks, we ask that they impute secondary marketing gains and capitalized servicing for their loans held for investment. This is not in accordance to GAAP, but ensures apples-to-apples comparisons across peer groups. Net interest margin on loans held for investment is excluded.

- This chart is a profitability roll-up of all four production channels – Retail, Consumer Direct, Broker Wholesale and Correspondent.

- Channel mix differs by peer group.

–Marina Walsh, CMB mwalsh@mba.org.