Black Knight: Homeowners Tap Equity at Highest Rate in 16 Years

Black Knight, Jacksonville, Fla., said lenders originated a record 4.4 trillion in 2021, including a record $1.7 trillion in purchase loans.

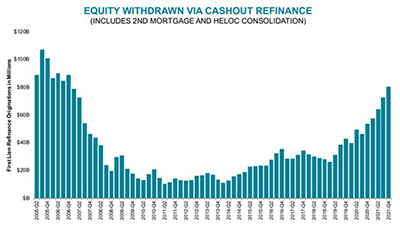

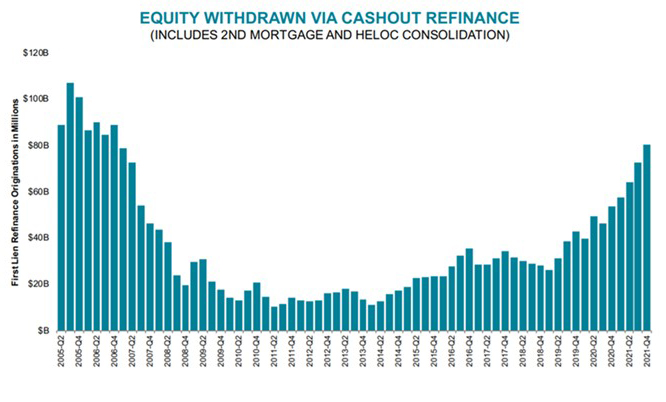

The company’s monthly Mortgage Monitor also reported while refinances fell by 34 percent last year to $2.7 trillion, homeowners tapped a record $275 billion in equity and $1.2 trillion in cash-out refinancings, the most since 2005 and just 1% short of a record high.

The report said in the fourth quarter alone, homeowners tapped $80 billion in equity, the larges quarterly volume in 15 years. More than one million homeowners withdrew equity via cash-out refinancings for the fifth consecutive quarter. The fourth quarter also saw the largest share of total available equity withdrawn since 2005, although the report noted homeowners are tapping their available equity at half the rate than at the prior peak.

“Entering 2021, consensus opinion was that originations would likely come in 20-25% lower than 2020’s record-breaking levels,” said Black Knight Data & Analytics President Ben Graboske.

The report said underlying risk remains low, with average credit scores above 740 and rising home values resulting in much lower post-withdrawal loan-to-value ratios than in years past.

Additionally, the report noted despite overall retention hitting an eight-year high in the fourth quarter, the retention rate on cash-outs is 8 percentage points below that of rate/term refis, in a market shifting heavily to equity-centric lending. On average, borrowers who changed lenders received rates just 5 basis points lower than those retained, a clear indication that – while important – pricing is not the only key to successful customer retention.

“Lenders and servicers that create a positive customer experience see greater loyalty and retention,” Graboske said. “Retention metrics also highlight the need for data-driven marketing strategies and portfolio analysis, especially with rate/term refinance incentive cut by 65% year-to-date and lenders competing for a shrinking pool of high-quality candidates. In a market dominated by equity-centric lending, it becomes paramount for lenders/servicers to be able to accurately identify borrowers who meet certain defined criteria and are most likely to tap into the record levels of equity, and then create targeted marketing campaigns personalized for those specific borrowers.”