Chart of the Week: Monthly Payroll Growth and Unemployment Rates

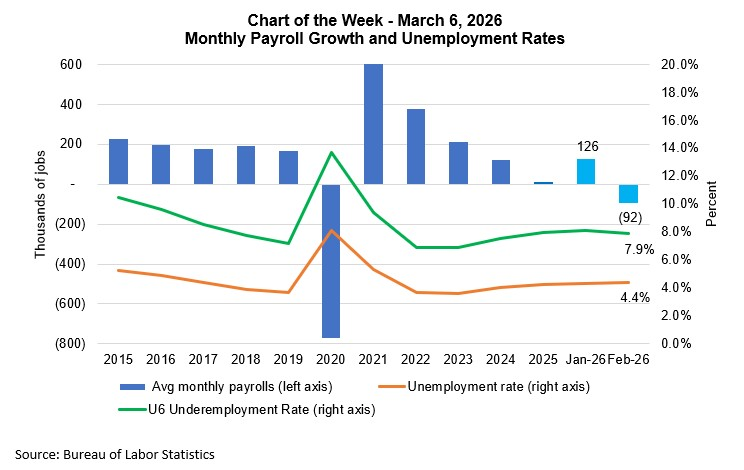

In 2025, job growth slowed to a crawl as the economy added an average of 10,000 jobs per month, and what little growth there was came from just a few sectors, notably health care. The diffusion index averaged 48.2 for all of 2025, meaning less than half of all industry sectors added jobs. In February 2026, with job losses in health care due to labor strikes, there was nothing left to support aggregate job growth, and total nonfarm payrolls declined by 92,000. Furthermore, job growth for December and January was revised down by a total of 69,000. Wage growth increased slightly to 3.8% over the past year.

The unemployment rate inched up to 4.4% in February as more workers re-entered the labor market but were unable to find work immediately. About one quarter of unemployed workers have been out of a job for more than 27 weeks and the average duration of unemployment increased to 26 weeks, the highest since 2022.

The job market is softening, and inflation is expected to increase due to a spike in oil prices resulting from the war in Iran. Even before the war began, PPI and PCE measures of inflation pointed to a reacceleration in inflation. Although this month’s job numbers were weaker than expected, we do not expect the FOMC to cut rates any time soon given the heightened inflation risk. MBA is sticking to its forecast that mortgage rates will remain in a range of 6 to 6.5% over the forecast horizon. A softer job market will be a headwind for housing demand as we enter the spring homebuying season.

• Mike Fratantoni (mfratantoni@mba.org); Joel Kan (jkan@mba.org)