MBA Chart of the Week: The Steepening of the Yield Curve in Multifamily Lending

Source: MBA CRE Mortgage Credit Availability Index (MCAI)

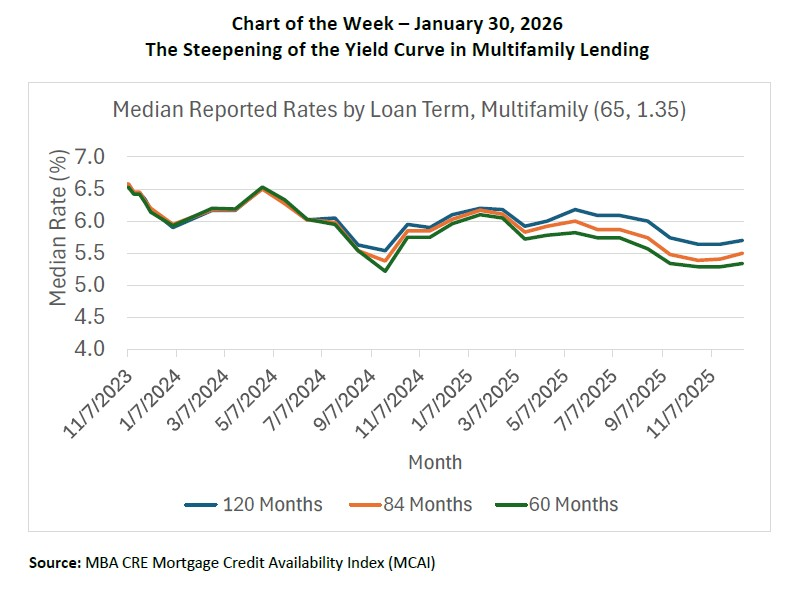

The yield curve steepened significantly from the end of 2024 and through 2025. The Federal Reserve cut rates three times in 2025, leading to a decline in short-term rates while long-term rates remained elevated.

This week’s Chart of the Week focuses on how the steepening yield curve is impacting multifamily lending. The figure uses data from the MBA’s CRE Mortgage Credit Availability Index and reports median rates at origination for three loan terms over time. We assume a constant loan-to-value ratio of 65 percent and a debt service coverage ratio of 1.35 at origination. The time series is reported for a loan term of 120 months (blue), 84 months (orange), and 60 months (green).

The figure shows that median rates were compressed through to August 2024, then began to widen slightly. Median rates widened further after the first rate cut in March 2025. This widening continued through to the end of the time series in 2025.

The steepening of the yield curve is shifting in lending patterns across multifamily and commercial real estate. Borrowers can shift from longer-term to shorter-term loans as the latter become relatively cheaper. We expect this trend to continue in 2026 and potentially into 2027.

The FOMC left the federal funds target range unchanged this month. However, we forecast one more rate cut toward the middle of 2026, which is likely to further steepen the yield curve. We expect originations to remain strong, given that multifamily and CRE borrowers can pivot to shorter-term loans. MBA Research forecasts growth in multifamily and commercial originations of 20.8 percent and 27.1 percent, respectively, in 2026.