CoreLogic: Mortgage Fraud Risk Drops by 3.1% Year-Over-Year

(Courtesy Corelogic)

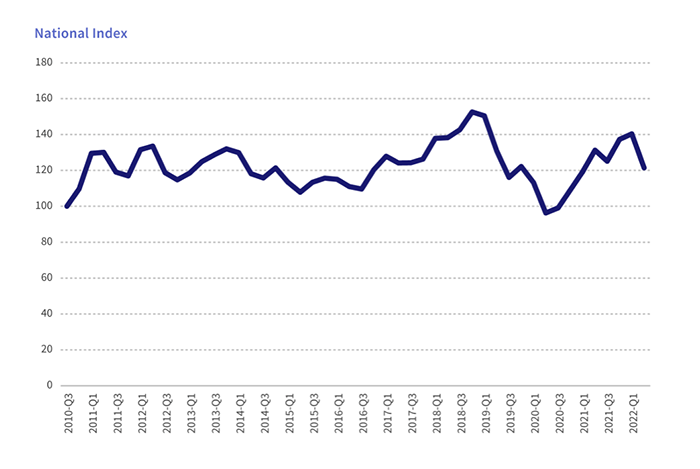

CoreLogic, Irvine, Calif., found that mortgage application fraud declined 3.1% year-over-year compared to the second quarter of 2022.

Despite the year-over-year decrease, there was a quarter-over-quarter increase of 1.6% of mortgage fraud from the first quarter of 2023 to the second, the CoreLogic Mortgage Fraud Report said.

“Fraud risk levels have been holding steady since last year,” said Bridget Berg, senior leader, loan solutions with CoreLogic. “The industry continues to have a very high share of purchases compared to refinances, likely driven by rising interest rates. The current environment makes errors, delays and repurchases more costly. Ultimately, these factors have spurred many lenders to enact more careful loan screening procedures.”

Berg noted top concerns include false income schemes, undisclosed debt and occupancy misrepresentation.

The report estimated that 0.75% of mortgage applications nationally–one in 134–had indications of fraud in the second quarter. While this shows relative year-over-year stability for the overall index, there were some changes within the various segments. Five out of the six types of mortgage fraud CoreLogic measures saw increases year-over-year: Identity fraud (up 12%), occupancy risk fraud (up 11.8%), income fraud risk (up 6.2%), transaction fraud risk (up 1.9%), and property fraud risk (up 1.8%). The exception continued to be undisclosed real estate debt which was down 17.3%, an even more significant decrease than seen in 2022.

New York and Florida have seen year-over-year decreases in mortgage fraud—down 6.23% and 1.08%, respectively—but remain the top two states for this risk. They are followed by Connecticut, California and New Jersey. Rounding out the top ten are Washington, D.C., Massachusetts, Texas, Illinois and Maryland, with Maryland, Illinois and Massachusetts representing new additions to the top ten in 2023.

Additional report highlights include:

Purchase transactions as a share of overall volume have grown from 70% in Q2 2022 to 76% in Q2 2023. Purchase segments showed higher risk than refinances.

There was a volume shift from conforming purchases (down 24%) to FHA purchases (up 14%). Both segments showed small risk decreases year-over-year, but risk levels are consistently 20% higher for FHA purchases. FHA purchase applications had a large increase in volume (over 40%) from Q1 to Q2 2023. Segments with increasing risk since Q2 2022 include 2- to 4-unit purchases (up 23%), 2- to 4-unit refinances (up 20%), jumbo refinances (up 7%), and jumbo purchases (up 3%).