Elevating Your Quality Quotient, Part II: Mortgage Servicing Post-Pandemic

Kristin Broadley serves as Chief Innovation Officer with QC Ally. She is responsible for identifying strategies, business opportunities and new technologies to enhance competitiveness. She previously spent 20 years with the Rocket Family of Companies serving in various roles. Kristin.Broadley@QCAlly.com.

Stuart Quinn has worked in housing finance, mortgage policy and technology in the private sector for more than 10 years. He joined Housing Finance Strategies in mid-2022 from Accenture to provide expertise on the landscape of fintech, mortgage modernization and housing policy. While with Accenture he served as a Product Manager focusing on platform integrations, GSE technology integrations, end-user experience and Loan Origination Systems. Prior to Accenture, he worked in Advisory Services as Policy Research and Strategy Analyst for CoreLogic. squinn@housingfinancestrategies.com.

Servicing Beyond the COVID-19 National Emergency

The Consumer Financial Protection Bureau was established in 2011 with expansive oversight of consumer financial services. The new agency folded certain mortgage servicer activities under their rulemaking authority. The agency oversight coverage includes both bank and non-bank entities performing servicing functions through the promulgation of amendments to the Real Estate Settlements Procedures Act (RESPA or Reg X) and the Truth-in-Lending Act (TILA or Reg Z).

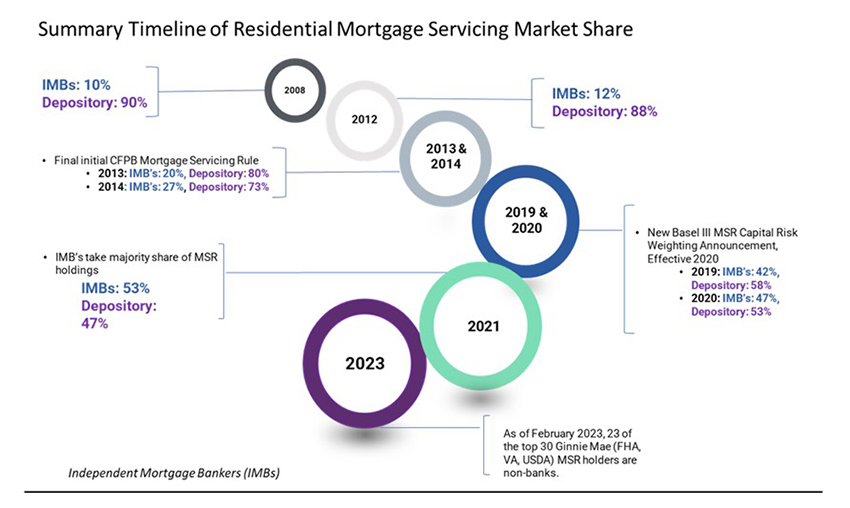

The initial round of final servicing rules released in early 2013 are now commonplace and executed on a second-by-second and minute-by-minute basis by mortgage servicing companies. For example, the rules sought to create standards around: general servicing entities maintenance of policies and procedures; periodic billing statements; notices related to interest rate adjustments for adjustable-rate mortgages (ARMs); timelines associated with payoffs; certain prohibitions of force-placed insurance; and escrow analysis requirements just to name a few. For delinquent or distressed borrowers, the rules also included regulation on early intervention, continuity of contact and protocols around loss mitigation communication routines and offerings. Since that time and in-between a number of regulatory clarifications, amendments and even the make-up of the servicing sector has rapidly evolved.

The Evolving Marketplace of Mortgage Servicing

Regulations offer guardrails, but rebuilding trust is key to a vibrant mortgage servicing industry. The hurdles of the Great Financial Crisis have been largely overcome and the COVID-19 Pandemic National Emergency was formally decreed behind us on April 10. [1] So, what does the marketplace for servicing look like today and what aspects of servicing could look different in the future?

Evolving Participants

“The high costs of origination and servicing along with the complexity of regulations create a costly business with significant legal, reputational and operational challenges. In addition, given capital requirements and the lack of a healthy securitization market, it barely makes sense for banks to hold mortgages or mortgage-servicing rights. Many banks have already reduced much of this business.

– Jamie Dimon, Chairman and CEO, JPM Chase & Co. [2]

Through a combination of regulatory changes, capital requirements, reputation risk and other factors, the entities who perform mortgage servicing have shifted since the creation of the original servicing rules. In many ways non-banks or independent mortgage banks (IMBs) offer advantages by being more technologically nimble, while operating under the same servicing regulations as banks. Banks, Credit Unions, Housing Finance Agencies and other participants continue to play an integral role within residential mortgage servicing, but at a much lower volume. In 2021 IMB’s had the majority share of residential service right holdings 53%, up significantly from just 10% share in 2008. The shift has been even more pronounced for Ginnie Mae (FHA, VA and USDA), who estimate 23 of the top 30 mortgage servicing rights (MSR) holders to be non-banks. [3]

Non-Performing Costs Remain Stubbornly High

In the first half of 2022, non-performing loan costs, on a per unit basis, were 12.5 times higher than the cost of servicing a performing loan. Many lenders are becoming more dependent on servicing revenue with the slowing expectations of originations in 2023 due to pressure from increased mortgage rates, a dwindling population of eligible refinances, and lack of existing and new housing supply. To preserve this revenue, servicers will need to focus on optimizing efficiency in order to manage costs while maintaining high levels of quality, customer service and execution aligned with company policies and procedures. Currently the Mortgage Bankers Association (MBA) estimates that three components of servicing account for nearly 50% of the costs: (i) Servicing Systems (18%); (ii) Customer Service (17%); (iii) Loss Mitigation (13%).

Announced Changes in Implementation Phase

With the formalization of the expiration of COVID-19 National Emergency by the Biden Administration both Fannie Mae and Freddie Mac (the GSEs) and other federal government mortgage credit investors have started to adapt their policies to support mortgage servicing in a post-COVID-19 environment.

Credit Investor and Insurer Regulatory Policy Changes

GSEs

Fannie Mae and Freddie Mac updated their guidance in mid-April when the GSE’s jointly announced updates to their servicing waterfall as it relates to servicer usage of Payment Deferral and Disaster Payment Deferral programs for distressed borrowers. [4.1][4.2] These rules become effective as early as July 1, 2023, but no later than October 1, 2023. Additionally, requiring servicers to evaluate their existing waterfall and technology to ensure support of the updated programs. Mortgage servicers will need to evaluate their population of eligible borrowers based on the updates which include: (i) existing distressed borrowers without a forbearance or repayment plan; (ii) those borrowers exiting a forbearance plan and; (iii) those borrowers have been unable to successfully complete an existing repayment plan. As with any significant change to procedures and loss mitigation process, mortgage servicers can benefit from self-examination and risk-based testing through QC and QA processes to measure success and risks associated with the updated guidance.

FHA, VA, USDA

The FHA, USDA and VA provided updated guidance to extend borrower eligibility to request a COVID-19 forbearance on April 7, April 10 and April 21 respectively. [5.1][5.2][5.3] Extending the intake date to May 31, 2023 will offer a welcomed transition period for mortgage servicer outreach, but also raises risks for servicers during the transition. For example, servicers will need to manage and address incoming new requests and extension requests from borrowers already within a forbearance plan that is scheduled to expire prior to May 31. In addition to the extension of the National Emergency programs, the FHA has also finalized a rule allowing for a 40-year modification, whereby lenders may be eligible to recast a borrower’s loan terms to offer further monthly payment relief. [6]

Changes Potentially on the Horizon

CFPB Guidance

Thus far, the CFPB has been relatively silent around formal guidance and regulatory changes related to the expiration of COVID-19. As the agency with authority over Reg X controlling certain loss mitigation requirements, it is not unfair to expect that the Bureau would review the language as amended rapidly under the outbreak of COVID-19 to put further assuredness around the regulatory requirements. Specifically, Reg X does not explicitly define what constitutes a complete loss mitigation package, nor what the components of the package should include. [7] As such, servicers need to be well versed in investor guidance and their own internal policies and procedures to ensure adherence to the regulation. Recent updates from the GSEs begin to formulate more explicit requirements around these definitions and offer an opportunity for the CFPB to formalize their previously issued joint statements and frequently asked questions (FAQ) released at the outset of the pandemic. [8][9] Finally, The Cares Act 2020 also set out a timeline for expiration of consumer reporting requirements under modifications to the Fair Credit Reporting Act (FCRA) statutorily expiring 120 days after the announced termination of the COVID-19 National Emergency. [10] Formal guidance around the transition and flexibilities for reporting remains outstanding.

Credit Investor Insurer Proposal In-Flight

Early outreach and expansive loss mitigation options were hallmarks of success related to the response to the COVID-19 National Emergency. Now that certain authorized options are scheduled to expire, there is an expectation that agencies evaluate additional options that may further benefit consumers dealing with non-disaster related hardships such as change in income or unemployment. FHA would benefit the most from swift action in creating new guidance around programs to backfill post-May 31 expirations given the recent uptick in their portfolio delinquency rates. Nearly 1 in 10 borrowers having missed at least one payment. Both industry and advocates have readily supported an FHA payment supplement account (PSA) which FHA has been receptive to. [11] To date, the agency has not issued formal proposed details around the mechanics of the program. Meanwhile, the VA can evaluate regulations controlling their repayment programs, which as written, requires the borrower to be 61 or more calendar days delinquent. An earlier intervention at 31 days could offer additional time for borrower evaluation and document intake if the hardship is related to unemployment or ongoing changes to monthly household income.

Conclusion

The 2023 mortgage origination environment will be challenging with the MBA estimating volumes to be down by 20% from last year, but servicing revenue remains a potential bright area for the mortgage business. [12] The expiration and reconfiguration of borrower eligibility for loss mitigation options creates an intensity of focus on addressing and adapting to the ongoing evolution of options. Updating processes and documenting the changes is one part of ensuring teams understand the changes and operationally execute in-line with the policies and procedures. Post-implementation testing ensures that the updated processes and policies are working as intended and required. It is impossible to forecast a pandemic, in the post-pandemic environment, risks and uncertainties can be easier to identify or predict. Then those risks can and should be identified, mitigated, and brought to resolution through continuous testing and evaluation.

Read Part I: Taking Stock of Mortgage Servicing in Three Acts

Citations:

[1]: President Joseph Biden, H.J. Res. 7, April 10, 2023, https://www.whitehouse.gov/briefing-room/legislation/2023/04/10/bill-signed-h-j-res-7/

[2]: Jamie Dimon, “Chairman and CEO Letter to Shareholders, 2022,” Section: Updates on Specific Issues Facing Our Company, April 4, 2023. https://reports.jpmorganchase.com/investor-relations/2022/ar-ceo-letters.htm

[3] Ginnie Mae, “Global Analysis Report,” Section 12: Holders of Ginnie Mae Mortgage Servicing Rights, April 2023. Note, data as of February 2023. https://www.ginniemae.gov/data_and_reports/reporting/Documents/global_market_analysis_apr23.pdf#page=49

[4.1]: Fannie Mae, “Lender Letter 2023-04,” Payment Deferral, Disaster Payment Deferral and Other Updates. April 12, 2023. https://servicing-guide.fanniemae.com/THE-SERVICING-GUIDE/Lender-Letter/2764017031/Lender-Letter-LL-2023-04-Payment-Deferral-Disaster-Payment-Deferral-and-Other-Updates.htm

[4.2]: Freddie Mac, “Bulletin 2023-8,” Issued March 29, 2023. https://guide.freddiemac.com/app/guide/bulletin/2023-8?_gl=1*1nrnn3u*_gcl_aw*R0NMLjE2ODM1NTc0MTIuQ2owS0NRand1LUtpQmhDc0FSSXNBUHp0VUYxSkZkb0x1NjQtaGRIbFg2SXVzMFJGNjl1ZkJ2VFN2ZXNWTnZhWWtDSkU5YzRzVVpOemlxTWFBblZmRUFMd193Y0I.*_gcl_dc*R0NMLjE2ODM1NTc0MTIuQ2owS0NRand1LUtpQmhDc0FSSXNBUHp0VUYxSkZkb0x1Nj

[5.1] Federal Housing Administration, “Mortgagee Letter 2023-08,” Extension for COVID-19 Forbearance and COVID-19 Home Equity Conversion Mortgage (HECM) Extensions Through May 31, 2023. April 7, 2023. https://www.hud.gov/sites/dfiles/OCHCO/documents/2023-08hsgml.pdf.

[5.2] U.S. Dept. of Agriculture Single Family Housing, “USDA Extends COVID-19 Forbearance Deadline to May 31, 2023.” April 10, 2023. https://content.govdelivery.com/accounts/USDARD/bulletins/35401f3.

[5.3] U.S. Dept. of Veterans, “Circular 26-23-08,” Forbearance Timeframe Extension for Borrowers Affected by COVID-19. April 21, 2023. https://www.benefits.va.gov/HOMELOANS/documents/circulars/26-23-08.pdf.

[6]: Increased Forty-Year Term for Loan Modifications, Federal Register, Vol 88, No., 45, [Docket No. FR–6263–F–02] (Mar. 8, 2023) (24 CFR Part 203). https://www.govinfo.gov/content/pkg/FR-2023-03-08/pdf/2023-04284.pdf

[7]: Marissa M. Yaker, Esq., Padgett Law Group, The Presidentially-declared COVID-19 National Emergency Ended. Here’s what it means for Agency-specific Loss Mitigation. Apr. 3, 2023. https://www.padgettlawgroup.com/plg-news/national-emergency-ended-heres-what-it-means-for-loss-mitigation

[8]: CFPB, FRS-BOG, NCUA, OCC, CSBS, FDIC (Inter-Agency), “Joint Statement on Supervisory and Enforcement Practices Regarding the Mortgage Servicing Rules in Response to the COVID-19 Emergency and the CARES Act (“Stickered”)”. Apr. 3, 2020. https://files.consumerfinance.gov/f/documents/cfpb_interagency-statement_mortgage-servicing-rules-covid-19_stickered.pdf. Hosted by CFPB, Accessed May 11, 2023.

[9]: CPFB, “The Bureau’s Mortgage Servicing Rules FAQs related to the COVID-19 Emergency,” Apr. 23, 2020. https://www.occ.gov/news-issuances/bulletins/2020/bulletin-2020-32b.pdf. Hosted by the OCC, Accessed May 11, 2023.

[10]: CFPB, “Statement on Supervisory and Enforcement Practices Regarding the Fair Credit Reporting Act and Regulation V in Light of the CARES Act (“Stickered”)”. Apr. 1, 2020. https://files.consumerfinance.gov/f/documents/cfpb_credit-reporting-policy-statement_cares-act_2020-04.pdf. Hosted by CFPB, Accessed May 11, 2023.

[11]: Center for Responsible Lending, Housing Policy Council, Bhagat, Kanav, “Payment Supplement: A Loss Mitigation Option to Provide Payment Relief for FHA Loans in a High Interest Rate Environment (November 18, 2022).” Available at SSRN: https://ssrn.com/abstract=4291125 or http://dx.doi.org/10.2139/ssrn.4291125 or https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-hpc-payment-supplement-fha-home-retention-opt-nov2022.pdf. Accessed May 11, 2023.

[12]: Mortgage Bankers Association, Mike Fratantoni, et al., “MBA Mortgage Finance Forecast (Apr. 17, 2023).” https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/2023/mortgage-finance-forecast-apr-2023.pdf?sfvrsn=399bbd96_1.

(Views expressed in this article do not necessarily reflect policies of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes your submissions. Inquiries can be sent to Michael Tucker, Editor, at mtucker@mba.org.)