Small-Cap Real Estate Conditions Dim

Small-cap commercial real estate market conditions have dimmed–and things will likely get worse before they get better, reported Boxwood Means LLC, Stamford, Conn.

“Last year’s halt to accommodating interest rates by the Federal Reserve, punctuated chiefly by a series of extraordinary increases in the Fed Funds rate targeting deepening inflation, has curbed the commercial real estate market’s expansion and long-standing stability,” said Randy Fuchs, Boxwood Means Principal and Co-Founder. “The winds have perceptibly shifted, now exposing investors and lenders to potentially widespread market and collateral risks unseen for about a decade notwithstanding the pandemic’s interregnum.”

Boxwood Means’ latest research report noted the damage to commercial real estate remains minimal in terms of loan delinquencies, defaults and distressed sales so far during this transition phase. “But with the doubling in commercial mortgage rates from last year, a more obvious, albeit slow-moving reveal is the major slump in commercial real estate lending–with perhaps the exception of the Agencies,” the report said. “Higher capital costs have frustrated the intentions of borrowers and killed countless deals. Anecdotally, many bank clients tell us their deal volume is about half of what it was last year. Couple this waning loan volume with a pullback in the investment sales market, and the commercial real estate market writ large may be heading toward further disruption or even recession in 2023–possibly in tandem with the U.S. economy as a whole.”

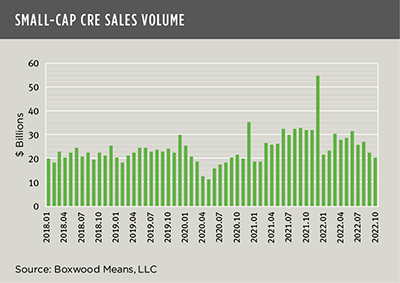

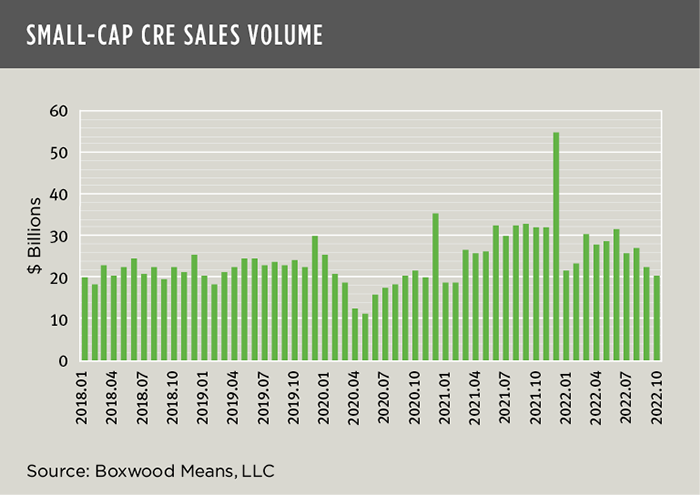

Fuchs noted collateral values worry both lenders and investors, “and are perhaps the main trigger for much of today’s market uncertainty.” Asset valuations have grown challenging as sales transactions have fallen with small-cap commercial real estate transaction volume (under $5 million in value) plummeting 37% year-over-year in October to the lowest monthly total in nearly two years. Similarly, MSCI Real Assets reported deal volume for principal transactions above $2.5 million dropped 21% versus the same period in 2021. Layer on shifting cap rates and less predictable property income, and we have increasingly poor visibility on prices, Fuchs said.

“If there is one, the silver lining to a painful, absolute decline in property values will be some restoration in market equilibrium and improved market liquidity, assuming, of course, that interest rates level off and the economy avoids a tailspin,” Fuchs said.