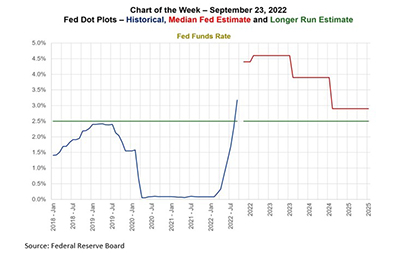

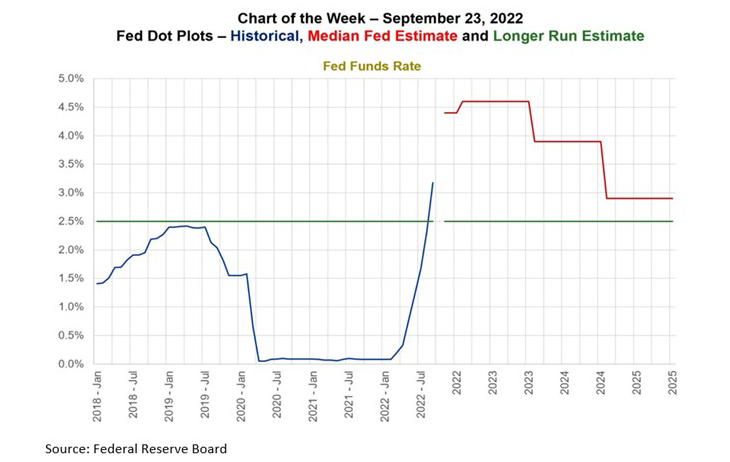

MBA Chart of the Week Sept. 23, 2022–Fed Dot Plots

In response to inflation continuing to run well above its target of 2%, the Federal Reserve this week again raised the federal funds target by 75 basis points. Now at 3%, the rate above what most FOMC members consider to be the long-term level and should be effective in reducing demand and slowing inflation over time.

No changes were made with respect to their ongoing plans to reduce the size of their balance sheet. Rate volatility is high due to both uncertainty regarding the Fed’s next moves and the lack of a steady, consistent buyer for Treasuries, and particularly mortgage-backed securities.

The FOMC members’ projections indicate slower growth, slowly decelerating inflation, and a fed funds rate that will likely top out well above 4%. The surprise for the market might be the median expectation that they could increase rates to 4.4% by the end of this year.

Mortgage rates have jumped the past few weeks following the August inflation report, which indicated that the Fed will continue to be aggressive in combating stubbornly-high inflation levels.

In fighting against persistently high inflation, the Fed is using the primary tool at its disposal, interest rates. The negative impacts of that inflation can be seen in residential and commercial development, where costs have been accelerating over the past year, making each new unit more expensive to build. The downside of the Fed’s actions, however, can also be seen in the fact that each bump in rates makes building and financing real estate more expensive, making it harder for new deals to pencil out.

The Fed’s actions have had a more pronounced effect on shorter-term than longer-term rates, but even so, the cost of long-term borrowing has just about doubled since the beginning of the year, leading to marked slowdowns in both residential and commercial borrowing and lending.

—Mike Fratantoni mfratantoni@mba.org; Jamie Woodwell jwoodwell@mba.org; Joel Kan jkan@mba.org.