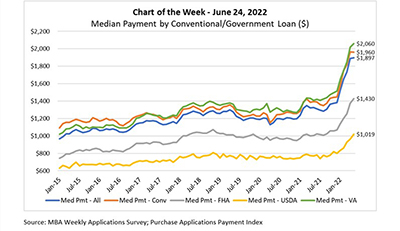

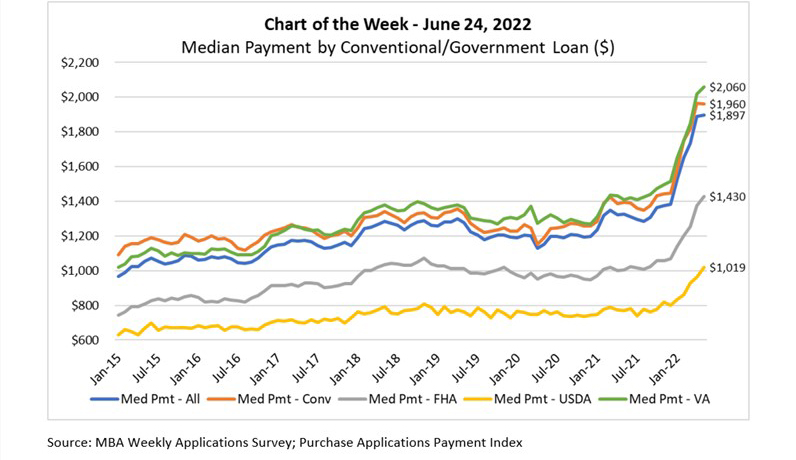

MBA Chart of the Week June 24, 2022: Median Payment by Conventional/Government Loan

The national median mortgage payment was $1,897 in May, a slight increase from $1,889 in April and $572 higher than in May 2021, according to this week’s Purchase Applications Payment Index release.

Payments have increased $513 (37.1%) in the first five months of the year, consistent with still-elevated loan sizes, as home prices remain high in many markets, and as mortgage rates surged from 3.7% in January to 5.5% in May. The ongoing affordability hit of higher home prices and fast-rising mortgage rates led to a slowdown in purchase applications in May, as potential buyers were either priced out of the market or decided to delay or adjust their search for a home.

This week’s MBA Chart of the Week captures that upward swing in median payments, along with additional details on median payments for the various loan types that make up the mortgage market. For example, the national median mortgage payment for FHA loan applicants, represented by the gray line in the chart, was $1,430 in May, up from $1,374 in April and $1,005 in May 2021. This 4.1% increase in FHA payments is of particular significance because many first-time home buyers utilize FHA mortgages to buy homes. Additionally, the national median mortgage payment for conventional loan applicants (orange line), the largest segment of the market, was $1,960, down from $1,967 in April but up from $1,394 in May 2021.

This month’s release also includes metrics on the impact of these payments relative to income growth. The national PAPI increased 0.4 percent to 163.4 in May from 162.8 in April, meaning payments on new mortgages take up a larger share of a typical person’s income. Compared to May 2021 (120.6), the index jumped 35.5 percent. An increase in MBA’s PAPI – indicative of declining borrower affordability conditions – means that the mortgage payment to income ratio (PIR) is higher due to increasing application loan amounts, rising mortgage rates, or a decrease in earnings. A decrease in the PAPI – indicative of improving borrower affordability conditions – occurs when loan application amounts decrease, mortgage rates decrease, or earnings increase.

Joel Kan jkan@mba.org; Edward Seiler eseiler@mba.org.