CoreLogic: Homeowners Gained $2.9 Trillion in Equity in Q2

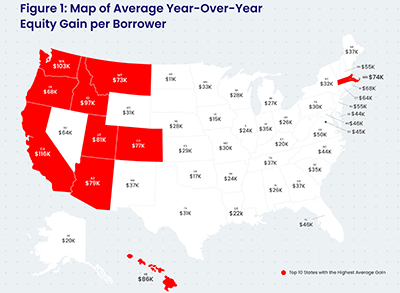

CoreLogic, Irvine, Calif., said homeowners with mortgages saw their equity increase by 29.3% year over year, representing a collective equity gain of more than $2.9 trillion and an average gain of $51,500 per borrower over the past year.

The company’s quarterly Homeowner Equity Report also reported mortgaged homes in negative equity–also known as underwater mortgage–decreased by 12% to 1.2 million homes, or 2.3% of all mortgaged properties.

“Home equity wealth is at a record level and will bolster economic activity in the coming year,” said Frank Nothaft, chief economist for CoreLogic. “Higher wealth spurs additional consumer expenditures and also supports room additions and other investments in homes, adding to overall economic activity.”

The report noted because of ongoing government provisions, increased vaccine availability–enabling many to return to work and a steady income–and record homeowner equity gains, most borrowers have been able to remain current on their mortgage payments. Additionally, the majority of borrowers that fell behind on payments have a large home equity cushion that will help them avoid foreclosure.

“The growth in homeowner equity provides a strong financial cushion for tens of millions of Americans. For those most impacted by the pandemic, equity gains will help play a critical role in staving off foreclosure,” said Frank Martell, president and CEO of CoreLogic.

Other report findings:

–1.8 million homes, or 3.3% of all mortgaged properties, were in negative equity. This number decreased by 30%, or 520,000 properties, in the second quarter.

–The national aggregate value of negative equity fell to $268 billion at the end of the second quarter, down quarter over quarter by $5.2 billion, or 1.9%, from $273.2 billion in the first quarter and down year over year by $18.9 billion, or 6.6.

The report noted because home equity is affected by home price changes, borrowers with equity positions near (+/- 5%) the negative equity cutoff are most likely to move out of or into negative equity as prices change, respectively. Looking at the second quarter book of mortgages, if home prices increase by 5%, 160,000 homes would regain equity; if home prices decline by 5%, 211,000 would fall underwater.