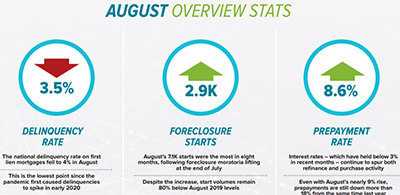

Black Knight: Strong Equity Could Affect Foreclosure Starts

Black Knight, Jacksonville, Fla., said even though just 7% of homeowners in forbearance have less than 10% equity after including 18 months of deferred payments, the potential for foreclosure activity persists.

The company’s monthly Mortgage Monitor report said while homeowners with limited equity were much more likely to be referred to foreclosure during the early stages of the Great Recession, foreclosure start rates on 120+ day delinquencies have been relatively similar regardless of equity position from 2010 on. However, high-equity borrowers are more than 40% less likely to face the involuntary liquidation of their home (via short sale, foreclosure sale, deed-in-lieu, etc.) than borrowers with weaker equity positions.

The report said even among borrowers with less than a 60% combined loan-to-value ratio, 30% of those referred to foreclosure ultimately faced involuntary liquidation. Black Knight Data & Analytics President Ben Graboske said this suggests many who could sell to avoid losing their home to foreclosure are not always doing so.

Complicating matters further, the report said, the white-hot housing market that has been driving increased equity stakes through rising home values has begun to show signs of cooling, albeit slightly. Annual home price growth slowed from an all-time-high of 19.4% in July to 19% in August, marking the first decline in the rate of annual appreciation in 15 months, with daily tracking data for September suggesting further cooling is on the way.

Graboske said this could prove to be welcome news for potential homebuyers, as the monthly payment required to buy the average priced home with a 20% down, 30-year fixed rate loan is the highest it’s been since late 2007, despite still historically low interest rates

“Holding equity in one’s home might not be a blanket backstop to foreclosure activity,” Graboske said. “Borrowers with limited equity were much more likely to be referred to foreclosure during the early stages of the Great Recession than those with strong equity positions. But foreclosure start rates on homeowners who were 120 or more days past due have been relatively similar regardless of equity stakes from 2010 on, with borrowers in the strongest positions only slightly less likely to be referred to foreclosure. So, while we may see some variation in foreclosure activity based on the equity levels of borrowers who are unable to return to making payments post-forbearance, those with strong equity won’t necessarily be immune to foreclosure referral.”

The report said buyers now require 21.6% of the median household income to make the monthly mortgage payment on the average home purchase, making housing the least affordable it’s been since 30-year rates rose to nearly 5% back in late 2018. Since the Great Recession, home price growth has begun to slow when such payment-to-income ratios hit approximately 20.5% or higher, but low inventory levels in recent months have led to record home price growth even with tightening affordability.