Share of Mortgage Loans in Forbearance Falls Under 4%

The share of mortgage loans in forbearance fell for the 16th straight week and is now under 4 percent for the first time since onset of the coronavirus pandemic, the Mortgage Bankers Association reported Monday.

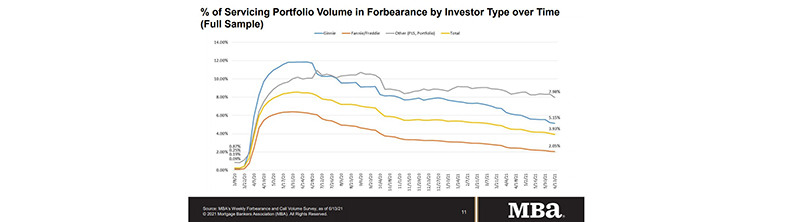

The MBA Forbearance and Call Volume Survey reported loans now in forbearance decreased by 11 basis points to 3.93% of servicers’ portfolio volume as of June 13, down from 4.04% in the prior week to 3.93%. MBA estimates 2 million homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased by 4 basis points to 2.05%. Ginnie Mae loans in forbearance decreased by 7 basis points to 5.15%, while the forbearance share for portfolio loans and private-label securities decreased by 35 basis points to 7.98%. The percentage of loans in forbearance for independent mortgage bank servicers decreased 16 basis points to 4.05%, while the percentage of loans in forbearance for depository servicers declined by 3 basis points to 4.16%.

“The share of loans in forbearance declined for the 16th straight week, with declines across almost every loan category,” said MBA Chief Economist Mike Fratantoni. “New forbearance requests, at 4 basis points, remained at an extremely low level. More than 44 percent of borrowers who exited this week used a deferral plan, highlighting the importance of this option.”

Fratantoni said as more homeowners reach the end of their forbearance term, “we should continue to see the share in forbearance decline. The improving job market and strong housing market are providing support for those who do exit.”

Key findings of MBA’s Forbearance and Call Volume Survey – June 7 – June 13

• Total loans in forbearance decreased by 11 basis points relative to the prior week: from 4.04% to 3.93%.

o By investor type, the share of Ginnie Mae loans in forbearance decreased from 5.22% to 5.15%.

o The share of Fannie Mae and Freddie Mac loans in forbearance decreased from 2.09% to 2.05%.

o The share of other loans (e.g., portfolio and PLS loans) in forbearance increased from 8.33% to 7.98%.

• By stage, 10.6% of total loans in forbearance are in the initial forbearance plan stage, while 83.5% are in a forbearance extension. The remaining 5.9% are forbearance re-entries.

• Total weekly forbearance requests as a percent of servicing portfolio volume (#) remained the same at 0.04%.

• Of the cumulative forbearance exits for the period from June 1, 2020, through June 13, 2021:

o 27.6% resulted in a loan deferral/partial claim.

o 24.1% represented borrowers who continued to make their monthly payments during their forbearance period.

o 15.3% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

o 13.8% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

o 10.2% resulted in a loan modification or trial loan modification.

o 7.5% resulted in loans paid off through either a refinance or by selling the home.

o The remaining 1.5% resulted in repayment plans, short sales, deed-in-lieus or other

reasons.

• Weekly servicer call center volume:

o As a percent of servicing portfolio volume (#), calls increased from 6.9% to 7.0%.

o Average speed to answer decreased from 2.0 minutes to 1.3 minutes.

o Abandonment rates decreased from 6.2% to 4.2%.

o Average call length remained the same at 7.8 minutes.

• Loans in forbearance as a share of servicing portfolio volume (#) as of June 13:

o Total: 3.93% (previous week: 4.04%)

o IMBs: 4.05% (previous week: 4.21%)

o Depositories: 4.16% (previous week: 4.19%)

MBA’s latest Forbearance and Call Volume Survey represents 74% of the first-mortgage servicing market (37.0 million loans). To subscribe to the full report, go to www.mba.org/fbsurvey.

If you are a mortgage servicer interested in participating in the survey, email fbsurvey@mba.org.