Murali Tirupati: Reducing Loan Defect Risks with Mortgage Document Automation

Murali Tirupati is a serial entrepreneur and cofounder & CEO of mortgage automation startup, Vaultedge (www.vaultedge.com), which helps mortgage lenders, servicers and investors automate document processing to reduce loan production, boarding & due diligence costs. He has 20 years of enterprise software consulting and sales experience. He has an MBA from Indian Institute of Management, Ahmedabad and a BS in Electronics & Communications Engineering from NIT, Trichy.

Introduction

Loan origination and boarding has largely been a manual and paper intensive process. Moreover, it has been observed over the past decade that loan production cost increased at a CAGR of ~7% whereas headcount productivity decreased by more than 50%!

This means that the loan origination & boarding process is not as efficient as it should be.

Typical loan files contain dozens of documents totaling between 250 – 400 pages with thousands of data elements that need to be verified and processed. Manual handling of such documents and data is slow and error prone. As these documents move downstream, crucial errors might creep in and that can render the loan file unserviceable. Such errors severely compromise loan quality and pose serious business risks to lenders and servicers.

In this article, we will analyze the bottlenecks due to a manual & paper intensive process that lead to loan defects. Based on this understanding, we will investigate the key business risks from such loan defects and how automation can play a role in mitigating these risks.

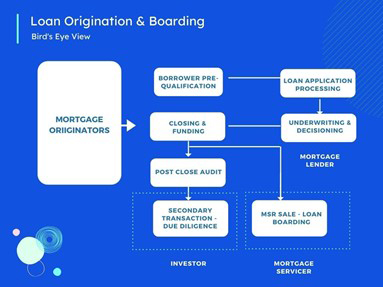

Overview of the Loan Origination & Boarding Process

Loan origination & boarding process is a complex one that involves multiple stakeholders & choke points. From a bird’s eye view, this is what the entire process looks like:

Mortgages are originated through multiple channels such as brokers, third party originators, correspondent lenders, co-issue, retail lenders etc. The origination process begins with the applicants submitting their employment details, financial statements and credit history for prequalification. Once prequalified, applicants enter the loan processing stage where they need to submit various documents that usually run into hundreds of pages. These typically include – their rental payments history, bank account statements, tax returns, pay stubs or W-2s, gift letters etc.

Once the loan documentation process is complete, it goes through the underwriting, credit decisioning, QC, loan funding & closure stages. After loan closure, separate loan assets & MSR assets are created. These assets undergo a post close audit when they are sent to a mortgage servicer for the sale of MSR. Alternatively, they undergo a due diligence process as a part of investor portfolio management.

At each step of the process – lenders, servicers and post close teams have to ingest bulk data in non-standardized formats (paper, scanned image, PDF, data feeds) & analyze them in a short span of time. This is a major bottleneck that can adversely impact loan quality and lead to serious business risks. Let us first understand these bottlenecks.

Understanding Bottlenecks that Lead to Loan Defects

1. People intensive processes – leading to lower output

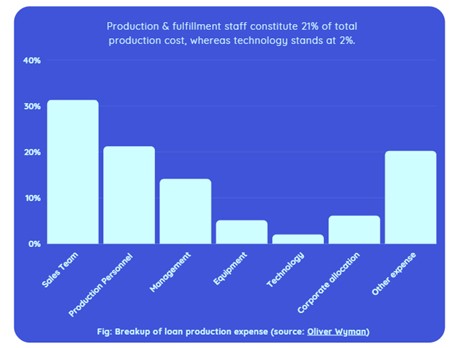

Mortgage origination & servicing operation has been inherently a people intensive activity. If we look at the breakup of production expenses, then we see that 66% cost can be attributed to personnel expenses. Production & fulfillment staff alone, accounts for 21% of the total cost.

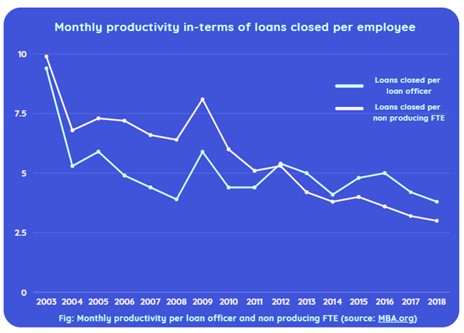

Ironically, people-heavy cost structure does not mean higher efficiency and better output. On the contrary, there has been a decline in average monthly productivity over the years.

The below chart represents the average monthly productivity for retail production between 2003 & 2018. It can be seen that during the period 2003 to 2018, there has been a steady decline of nearly 60% in the non-producing retail FTE productivity and monthly loan officer productivity.

Thus, loan production being largely a people driven process is experiencing a significant drop in per person output.

2. Document indexing is time consuming & cumbersome

Document classification, sorting and validation is one of the most time-consuming components of the loan origination & boarding process. On an average, it could take anywhere between 10 to14 days to complete these tasks, when done manually.

This is because loan packages consist of multiple types of documents running into hundreds of pages in different formats. In a manual process it is very difficult to judge the veracity of 500 complex pages of information in a short time and to do it repeatedly!

Thus, in a high loan volume environment, manual indexing could soon result in declining productivity.

3. Data validation and updation is error prone

A big challenge with the loan package is that – a large portion of documents, even if digitized, are printed out during loan origination, closing and boarding stage. Any manual data entry or updates in the paper documents, makes it difficult to maintain a proper version control. This can cause mismatch in data fields between paper documents and digital file in the loan origination system.

Another challenge stems from inaccuracies in data validation. A typical loan package of 250-400 pages in formats ranges from digital documents like – scanned PDF, excels to paper documents like photo ID copies. Each such package consists of thousands of data fields that need to be validated. However, manual data validation has two core challenges:

–First, when done manually, it is very difficult to track changes in customer data and update it uniformly across all the relevant documents and sub-systems.

–Second, federal & GSE regulatory compliance processes are embedded throughout the origination and boarding process. At each mandatory compliance step, new data must be collected and added to the core lending systems. With manual handling, updating data points as per compliance requirements becomes error prone.

Thus, manual handling of documents and data is cumbersome, inefficient & error prone. This becomes one of the main drivers of poor loan quality.

Business Risks Due to Loan Defects

A. The problem of poor loan quality and business risks

Loan quality refers to loan files containing accurate and sufficient documentation that complies with pre-determined loan policies of an originating lender, loan guarantor, loan investor, and/or regulator. Any aspect of the loan asset that does not conform to these pre-determined standards are called loan defects.

Thus, loan quality is measured in terms of number and severity of such defects. Higher the number and severity of defects, poorer is the quality of loans. It leads to two major business risks for all the stakeholders in the loan production and boarding value chain:

- Buy Back risk for lenders

Defective loans could be sent back to lenders for correction. In the worst case, there could be buyback requests from investors.

2. Financial risk for lenders & servicers

Lengthens the loan processing and boarding cycle, reduces per employee productivity of overburdened staff and increases overall production costs. Thus, we observe that bad loan quality due to defects is a major driver of business risks. In order to mitigate these risks, let us look at them in depth.

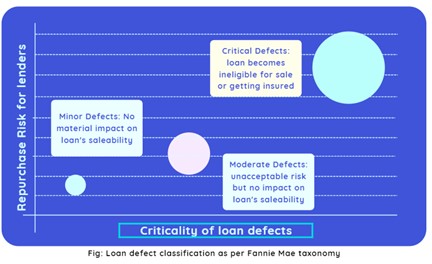

B. Buyback risks due to critical defects:

FHA & Fannie Mae loan defect taxonomy prescribes three severity levels of risks (as shown below).

Out of the three, critical defects are the ones that pose serious buy-back risk as they render a loan package ineligible for sale. Consequently, a lender has to provision for losses associated with non-saleable loans. From a mortgage servicer’s perspective, critical defects translate into non-compliance issues and penalties levied by external auditors & regulators. In order to understand the severity of this risk, let’s analyze some interesting trends –

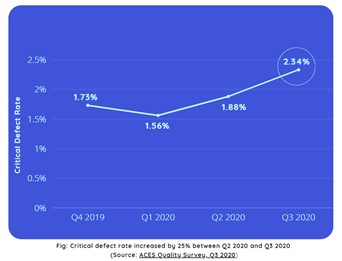

- Critical defect rate has increased over the past year

It is worth noting that overall critical defects have shown an upward trend in the last one year. As per the latest survey conducted by ACES quality management, the overall critical defect rose by 25% from Q2’s 1.88% to 2.34% in Q3 2020.

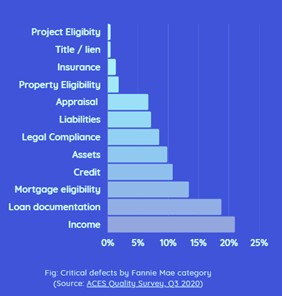

2. Loan documentation is the second largest source of critical defects

If we are to look into the key drivers of critical defects, then we see that loan documentation forms the second largest contributor at around 19% of all critical defects in Q3 2020.

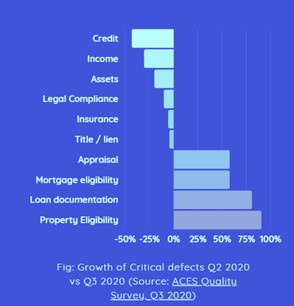

c. Critical defects due to loan documentation grew by 80%

If we compare the growth in critical defects within each category, we see those critical defects due to loan documentation has seen an increase of 80% between Q2 2020 & Q3 2020! Thus, loan documentation remained one of the major sources of critical defects in FY 2020.

To summarize – critical defects have increased during FY 2020-21, where errors in loan documentation process proved to be the second most important driver of such defects.

C. Financial risk due to operational overburden

Critical defects also pose formidable financial risks for lenders and servicers.

Lenders:

- Pricing adjustments associated with loan quality.

- Capital provisioning for defective loans

Servicers:

- Penalties for non-compliance

- Risks of possible early payment default and foreclosures

Another important, yet overlooked aspect is the cost of re-working a defective loan.

With 30-year fixed interest rates still low at 3% and a housing inventory shortage, demand & loans volumes are expected to stay high during FY 21-22.

Interestingly, ACES has observed that increased manufacturing-related problems has a direct correlation to underperformance issues. This means, higher the volume of loans manufactured, greater the possibility of defective loans. Thus, loan production and quality assurance teams are likely to remain overworked under a huge stockpile of loan volumes. Any re-work of defective loan files will further stretch the employees beyond their already surpassed capacities.

This will only result in further dip in productivity and rising loan production cost. An analysis of historic loan production cost based on the data of MBA.org, it has been observed that loan production cost has seen a steady increase, from $ 3600+ in FY 09 to $ 7500+ in FY 20.

This trend is expected to exacerbate further if critical defects continue to bog down the existing resource bandwidth of lenders & servicers.

Loan Defect Mitigation: A Case for Document Automation

Let us understand how document automation can reduce the above-mentioned risks in the entire process.

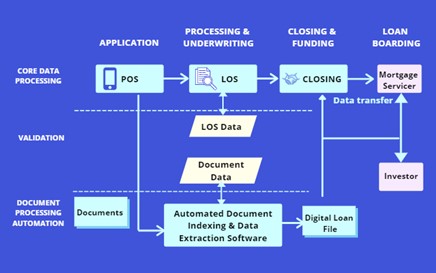

In the above figure, there are three workflows sitting on top of one another. In the core data processing workflow, LOS is the primary tool for the loan processors and underwriters. It ingests data from point of sale and multiple data sources like banks, credit agencies etc. Concurrently, document processing workflow sits in parallel to LOS and ingests data directly from the point of sale. However, it offers functionalities that LOS doesn’t offer.

Document automation software automatically captures, indexes, classifies and stores documents. It then extracts data from both structured and unstructured documents. Further, as a part of the validation step, it compares these data points with those from the LOS.

It also collects & manages new version of documents that ensures consistency with LOS data. Most importantly, it enables the lender/ servicer to identify exception and automate their resolution. This is critical because manual exception processing is slow, expensive and error prone.

Finally, integrating a document automation software with LOS can build and deliver error free digital loan-packages to mortgage servicers, investors, document custodians and others. In a nutshell document processing automation mitigate loan defect risks by:

- Automatically & accurately capturing & indexing various document types & formats.

- Extracting data from these documents & validating with LOS data. It allows proper version control & automated exception handling. This minimizes the chances of missing data, wrong entry or manual data entry

As a consequence, critical defects along with accompanying buy back risks and financial risks, adequately mitigated.

Document Processing Automation: Core Capabilities

Since we have understood the significance of integrating document automation software with LOS to improve loan quality & reduce business risks. Let us look at the core functionalities of such a software to aid proper evaluation.

Document Recognition & Classification

This involves automating identification of different doc & forms – 1003, pay stubs, deed of trust, W-2 etc. This is followed by indexing the pages mapped to the appropriate document types. Then, these documents are checked against a dynamic checklist to identify missing documents.

Document Construction

The system should provide a simple UI to view pages sorted by document type while separating out & labelling individual forms & documents.

Data Verification & Exception Handling

The capabilities for data extraction allow data to be collected from the mortgage file with both structured and unstructured data. Software platforms can extract more than 2000 data points from the ingested data set & assign a confidence score and a label (color code) to indicate whether it needs user review or not. Users can review these highlighted data points by simply clicking on the extracted value, to cross check the error.

Conclusion

From our analysis, we observed that the manual and paper intensive nature of the loan production process is the fundamental cause of critical loan defects. These defects pose buy back and financial risks to lenders and servicers. However, a document processing automation software, when integrated with the loan origination system can minimize such risks. They offer four core functionalities – automated document indexing, automated data extraction & validation, faster resolution of exceptions and delivery of error free loan packages to servicers/investors. In some situations, manual interventions can be reduced by 80%-90%, thus freeing up locked human capital while eliminating buyback and financial risks. In other words, document processing automation is a low risk and high reward strategy that can result in significant risk mitigation and productivity improvement across the entire loan production & boarding process.

(Views expressed in this article do not necessarily reflect policy of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes your submissions. Inquiries can be sent to Mike Sorohan, editor, at msorohan@mba.org; or Michael Tucker, editorial manager, at mtucker@mba.org.)