Dennis Postlewait of HCL Technologies: Next-Gen Lending Solutions for Efficiency and Cost Optimization

Dennis Postlewait is Director of Digital Process Operations with HCL Technologies, Highlands Ranch, Colo. HCL Lending Solutions assists lenders in moving away from legacy and monolithic systems to a host of digital platforms, including business process management workflows and robotic process automation to facilitate the true transition toward digital.

The digitization wave has significantly altered business models across several industries today. Digital laggards are trying their best to streamline operations with holistic process transformation in the new normal. Consumer expectations have vastly altered in tandem with simplifying operations and elevated user experiences through process transformations.

But how has digital transformation permeated across loan and mortgage services, and how can experienced partnerships prove valuable? We shall try to examine the current state of the industry and highlight the role of transformation partners in this blog.

The current state of the industry

There is a substantial gap in terms of true lender transformation in loans and mortgages. This distinct lack of process transformation has impeded any productivity improvement; as legacy processes have sustained for the past three decades. In most cases, any usage of technology is aimed at maintaining compliance and regulatory standards rather than being a future-facing process enabler.

One of the foremost reasons the industry has lagged can be attributed to the reluctance and resistance offered by the leadership, especially with medium to smaller organizations. Their primary concerns arise from:

• Lack of familiarity in case of transformed process and workforce

• Loss of control over processes to technology

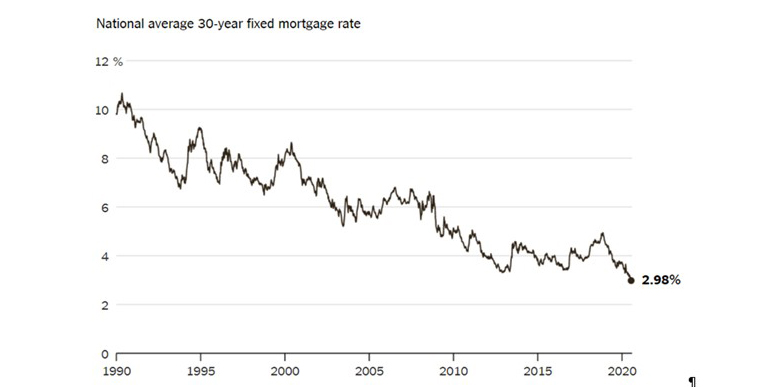

As a result, the average US mortgage market rates dropped to less than 3% for the first time in July 2020, which has the potential to cause a spurt in residential loan applications. This, combined with the fact that several mortgage organizations are still banking on legacy processes, can potentially complicate the scenario with sheer volumes. Unsurprisingly, it becomes a business imperative for industry leaders to leverage process transformation towards a digitally native operational structure that is substantially more efficient and agile.

Future-ready transformation partnerships

But how do overburdened lenders take up such a radical transformation? The good news is that organizations can partner up with digital transformation experts with expansive industry knowledge as well as rich and relevant experience. HCL’s team of digital process operations for consumer lending boasts extensive lending and servicing experience ranging from processing and verification services to complex underwriting work and from collections to bankruptcy and foreclosure management. HCL aims to assist and transition lenders to a significantly more agile and efficient operational framework in the face of increased lending volumes while keeping up with regulatory and customer expectations.

One of the key critical aspects of handling larger volumes is to bolster the team by onboarding new team members. Lending organizations running legacy processes often lack proper training and documentation for the onboarding process. Moreover, the lack of operational expertise often results in significantly longer onboarding timeframes, including up to 90-120 days for role assignment. HCL aims to address this by working within set timelines as processes get streamlined. The team is proficient in blending the tenets of process transformation with lending domain expertise. With this, they integrate continuous process improvement via detailed suggestions with standard process operations while ensuring stringent and specific guardrails for quality.

From a lender’s perspective, working with an experienced team of transformation professionals has stark business benefits. They can be summarized as:

• Control and transparency: HCL mortgage lending transformation is platform-agnostic, and the personnel are trained to work within the client’s loan origination system. This enables complete visibility across the entire loan management chain with absolute process transparency and ensures that lenders have complete control over every aspect.

• Savings on operational costs: The HCL team of experts helps clients with significant margin assistance through improved business process management. Streamlining of processes such as onboarding reduces costs significantly owing to shorter turnaround times and process standardization. Lenders also save on additional staffing as HCL supplements manpower and offers unit-based pricing regardless of volumes handled.

• Faster processing times: As discussed, the highly experienced team at HCL enables significant process improvement and operational efficiency with process standardization. Moreover, the constant identification and addressing of roadblocks ensure that operations are devoid of any elements that induce inefficiency.

• Enhanced user experience: The process optimization and simplification translates to lenders offering better services to their clientele (borrowers). Moreover, a strong quality control initiative and expansive experience ensure all operational blind spots are covered and complete security for both lenders as well as borrowers.

Fueling digital revolution in lending operations

The tomorrow of lending solutions will be driven by how effectively solutions providers help their clients adopt the right digital transformation tools in the correct parts of their business. This would help them achieve a meaningful enhancement in agility, flexibility, and productivity – such that they remain operationally customer-focused while also fostering a resilient future-ready posture.

(Views expressed in this article do not necessarily reflect policy of the Mortgage Bankers Association, nor do they connote an MBA endorsement of a specific company, product or service. MBA NewsLink welcomes your submissions. Inquiries can be sent to Mike Sorohan, editor, at msorohan@mba.org; or Michael Tucker, editorial manager, at mtucker@mba.org.)