MBA Chart of the Week: CRE Delinquencies and Net YTD Charge-offs at FDIC-Insured Firms

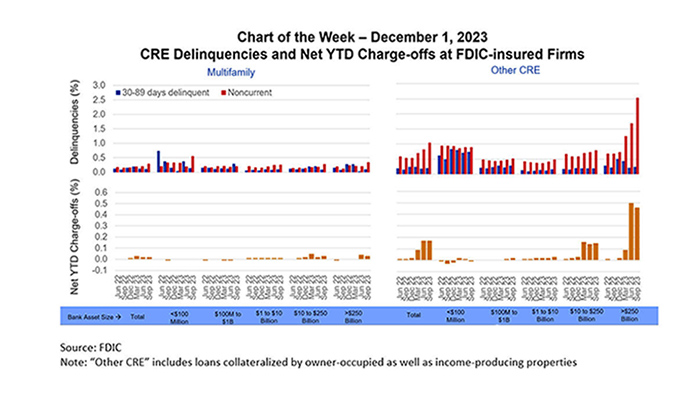

Source: FDIC

Note: “Other CRE” includes loans collateralized by owner-occupied as well as income-producing properties

Since March 2023, a recurring set of questions has revolved around a) how conditions in commercial real estate are affecting banks and b) how conditions with banks are affecting CRE. A variety of MBA Charts of the Week – including here, here and here – have delved into the topic and we do so again today, digging into some just released numbers from the FDIC’s Quarterly Banking Profile.

There’s a lot going on in this week’s COTW, so first a guide to the graphic. The chart presents information on the performance of FDIC-insured institutions’ holdings of multifamily mortgages (the left two charts) and other CRE-backed loans (the right two charts). Unlike many of MBA’s other series, the “other CRE-backed loans” featured in the graphic includes loans backed by owner-occupied as well as income-producing properties.

The graphic shows, in the top two charts, the dollar share of loans that are 30-89 days delinquent (in blue) and the share that are “noncurrent” (in red), which includes not only loans that are delinquent 90 or more days but also loans that are in “non-accrual” which brings in situations in which payment in full of principal or interest is not expected. The bottom two charts show the net percent of loans that banks have charged-off (year-to-date) because they do not expect to be paid back in full.

The chart breaks the results out by bank size (in terms of assets held – see the categories at the bottom shaded in blue) and covers quarterly figures from June 2022 to September 2023.

What are the key takeaways?

There has been a slight uptick in the noncurrent rate of multifamily loans, but the performance remains generally strong. And smaller banks and larger banks are reporting relatively consistent results.

Regarding other CRE-backed loans, the noncurrent rate has diverged significantly from the share of loans that are in early-stage delinquencies, likely a result of banks looking into their books and “taking their lumps” on loans that are still current but about which the banks have doubts. (MBA’s own survey of commercial mortgage delinquency rates saw Q3 office delinquency rates top those of retail and hotel properties for the first time since the survey began at the onset of the pandemic.) And there is a major divide between larger banks and midsize and smaller firms. The same is true for net charge-offs.

There are 14 firms in the largest-bank category, 142 in the next largest group and more than 4,400 in the remaining three categories.

So why, in recent quarters, have the larger banks increased the share of non-multifamily CRE loans they have characterized as non-current and charged-off, while smaller banks have not?

It is not hard to imagine that larger banks are facing greater scrutiny from investors and regulators, pushing them to react to the current uncertainty in parts of the CRE markets (think particularly office) and sock away funds for any eventuality. As one bank CFO commented on their Q3 earnings call, “And then I think most importantly, something that we control is our efforts to get ahead of the CRE office risk. So, in Q3, we were very intentional about working through moving from just identifying the risk there to actually resolving several of the problem credits. And we took some losses there to do that.”

It’s also not hard to imagine that many of the CRE loans on larger firms’ balance sheets are quite different from those held by smaller institutions. For example, the top 14 banks accounted for one-in-eight multifamily loans made by banks in 2022 but half of the multifamily loans greater than $100 million. Boxwood Means and others have detailed differences in performance between larger and smaller CRE properties in today’s market.

Higher interest rates, challenges for some properties and uncertainty about valuations all continue to stymie commercial real estate transaction activity. In the meantime, banks are working through their books, with banks remaining an important source of capital for CRE, and CRE debt remaining an important asset for banks.

Jamie Woodwell (jwoodwell@mba.org)